BOUGHT: Anexo Group Plc – 22% 5Yr Historical CAGR, 10x Current EV/EBIT

BOUGHT: Anexo Group Plc – 22% 5Yr Historical CAGR, 10x Current EV/EBIT

I’ve been a shareholder in Anexo Group Plc since April this year, a company offering credit hire services & legal services to victims of non-fault vehicle accidents, and earlier this month I added to my position following a drop in share price. In this piece, I’ll explain why.

Last week private equity group Dbay Advisors, who already own a 29% share of the business confirmed it would not be making a formal takeover offer after talks with management, which were reportedly revolving around a figure of £1.50 per share, fell through. To tell the truth, when the figure of £1.50 was being thrown around, I was a little disappointed. It seemed to be private equity doing their thing and getting a great deal for themselves, so when it was confirmed that the deal fell through, I was pleased. The market reacted badly, however, with the share price falling around 10% to around £1.30, and on the back of this I took the opportunity to reassess and added to my position.

To summarize the key risks & advantages I have concluded from my research:

Advantages

My multi scenario model, with special consideration of risk of default, results in fair value between 26% & 48% above the current SP;

The business performance has little correlation with the performance of the wider economy, offering genuine diversification;

The business has been growing at speed, with revenue growing at a CAGR of 22% over the last 4 years;

Backlog of 20,000 cases following impact of COVID-19 provides strong pipeline of revenue;

Management still has a controlling ownership in the business, with the joint shareholding of Alan Sellers (Chairman) & Samantha Moss (MD of Bond Turner) exceeding 50%;

Continued interest from private equity (who currently own 29% shareholding) provides a strong indication of value in the business;

Market share currently only 2.5%, providing ample room for further expansion;

Relatively low P/B ratio of 1.4x, which is due to large amount of working capital required in the business.

Key risks

The business model is underpinned by a ruling by the House of Lords whereby non-fault accident victims have the right to recover credit hire rates from third party insurers, there is therefore a key risk that further developments in case law disrupt the business;

Risk of further approaches from DBAY at undervalue.

The business model

The company, based in Liverpool in the UK, operates a business model whereby they assist in legal claims associated with non-fault vehicle accidents, and it specializes in impecunious legal claims. An impecunious claim in this context essentially means that the party making the claim does not have the financial means to source a replacement vehicle (think of the scenario in which a local tradesman gets into an accident, and can’t afford to purchase a replacement vehicle which they need in order to work).

The services offered by Anexo in this scenario are twofold: 1) Anexo will assist the claimant in sourcing a replacement vehicle via a credit agreement (this part of the business is called EDGE), and 2) Anexo will process the legal claim against the relevant insurance company to resolution (through its wholly-owned firm of solicitors Bond Turner). To illustrate, this diagram was provided in the Anexo year-end results:

Anexo charges fees associated with both the credit agreement in place with respect to the vehicle, and fees associated with processing the legal claim. The company operates on a “no win, no fee” basis, and therefore a key risk to the business is the success rate of legal claims undertaken. However, a good thing about this area of the legal sector is that the cases are high volume and low value, meaning the risk is well distributed and the cases are typically very standard in nature. As such the failure rate when cases go to trial is below 2% and in fact the vast majority of cases are settled before trial.

The main area of weakness that is inherent in the business model is its vulnerability to further changes in the law. The existence of the business is predicated on a series of House of Lords rulings which set precedents for what rights impecunious claimants have in a vehicle accident situation. Though the leading case with regards to this dates back to 2003 (Lagdan vs O’Connor, https://publications.parliament.uk/pa/ld200304/ldjudgmt/jd031204/lagden-1.htm), further developments continue to unfold (https://www.blmlaw.com/news/to-be-or-not-to-be-impecunious-that-is-the-question), and there is a risk that further developments significantly damage the ability of Anexo to earn revenue.

The DBAY offer

Last year DBAY purchased a 29% shareholding from management, and earlier on this year it was announced that they were in talks to make an offer for a complete takeover. However, a few weeks ago these talks fell through and no formal offer was made. The market reacted badly to this news, which is why I ended up putting this analysis together, however a key question to answer around this is, why didn’t the deal take place?

The concern is obviously that there might have been some performance issues or something else which put DBAY off, and admittedly information on exactly what happened is very hard to find.

However, drawing attention to the statement released by Anexo “Since [the initial announcement was made to the market], discussions with DBAY have not led to an offer which, in the view of the board, reflected the value of the company, and which the board therefore would have felt able to recommend to shareholders…”

From my point of view, it feels like there simply wasn’t agreement on the low pricing which DBAY were looking for, and so I don’t take this as being a warning sign, though I’d be happy to hear if anyone thinks differently…

COVID-19 Impact

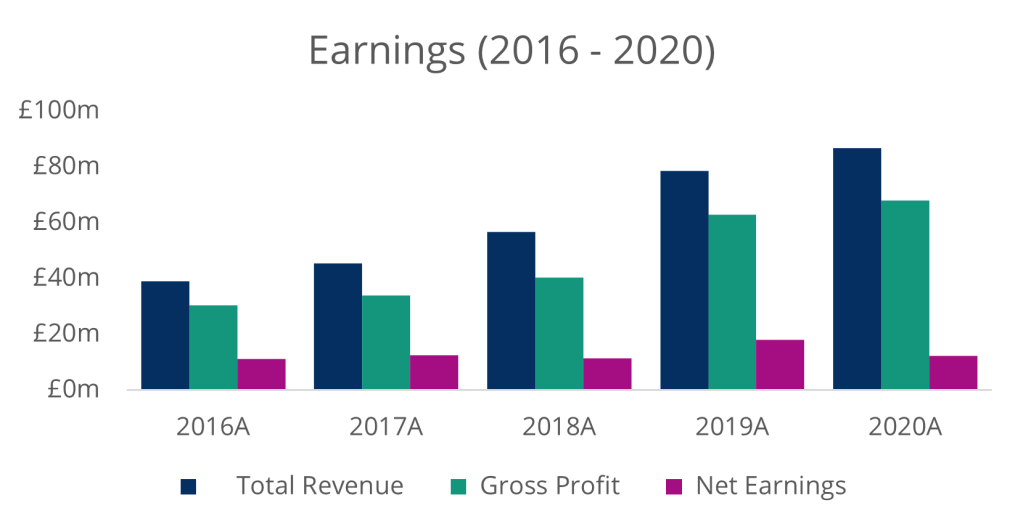

As noted earlier, the operations of Anexo are considered an essential service in the UK which has been highly beneficial to the business in reducing the amount of disruption that has occurred following the COVID-19 pandemic. That said, the business has still had its challenges in this environment, not least because its business is reliant on the legal process, which has been heavily clogged up because of disruption. As such, Anexo noted in its year-end results for 2020 that there were approximately 20,000 cases in the backlog, which is essentially revenue waiting to unwound.

Anexo did managed to increase revenue from £78.5m in 2019 to £86.8m in 2020, as part of the company’s effort to continue expanding, however there is clearly further room to improve this given the above and the reduction in fleet utilization seen from 2019 to 2020.

The company did see a slight reduction in gross profit in 2020, primarily because of increased operating expenses associated with:

Further expansion (see increase in staff numbers above);

Investment in VW emissions cases following court ruling against VW associated with manipulation of emissions tests.

The increased spending in terms of staff numbers represents a step change which will serve as a platform for further revenue expansion. Overall this kind of business has proved resilient to the COVID-19 environment, and I believe it will prove resilient through other downturns as well.

DCF Valuation

Normally I would look to talk through the historical performance and the outlook for the business before moving onto my model, but actually I think the best way illustrate these is to integrate it to the model explanation itself, so in this section I’ll talk through my process around each key variable.

I have valued the business based on the following 4 scenarios, with probability weightings:

1. Base Case (assigned 45% weighting)

2. Upside Case (assigned 22.5% weighting)

3. Solvent Downside Case (assigned 22.5% weighting)

4. Severe Downside (insolvency, assigned 10% weighting, nil recovery)

For each of these scenarios, with exception to the Severe Downside, I have built a separate DCF with differing assumptions which I shall talk through. The severe scenario has been assessed as having nil value, with the purpose of it being to explicitly consider the risk of legislative/legal changes which result in insolvency.

I would stress that using a multi scenario model like this is not useful because one can accurately assign scenario probabilities, but because this exercise will reveal if an upside or downside outcome has a significantly asymmetric impact on valuation.

Revenue

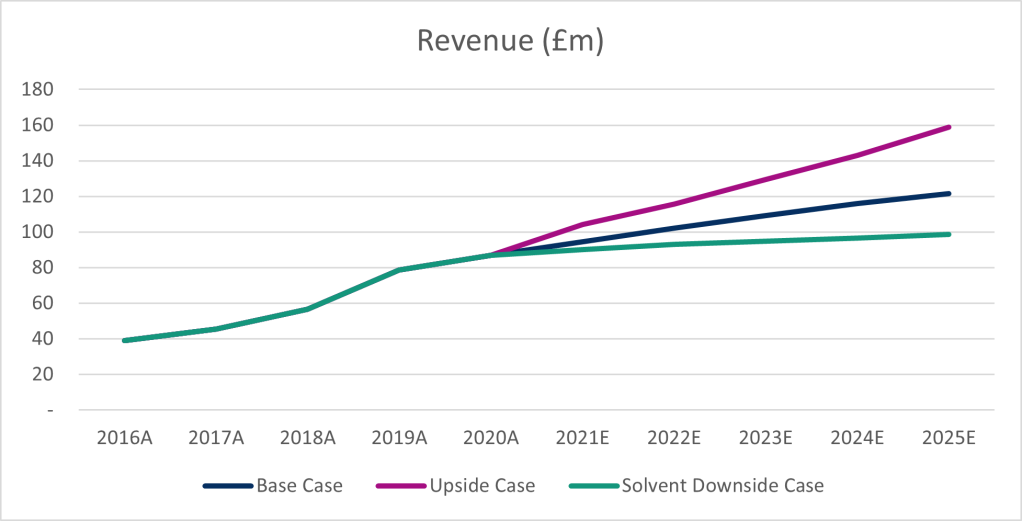

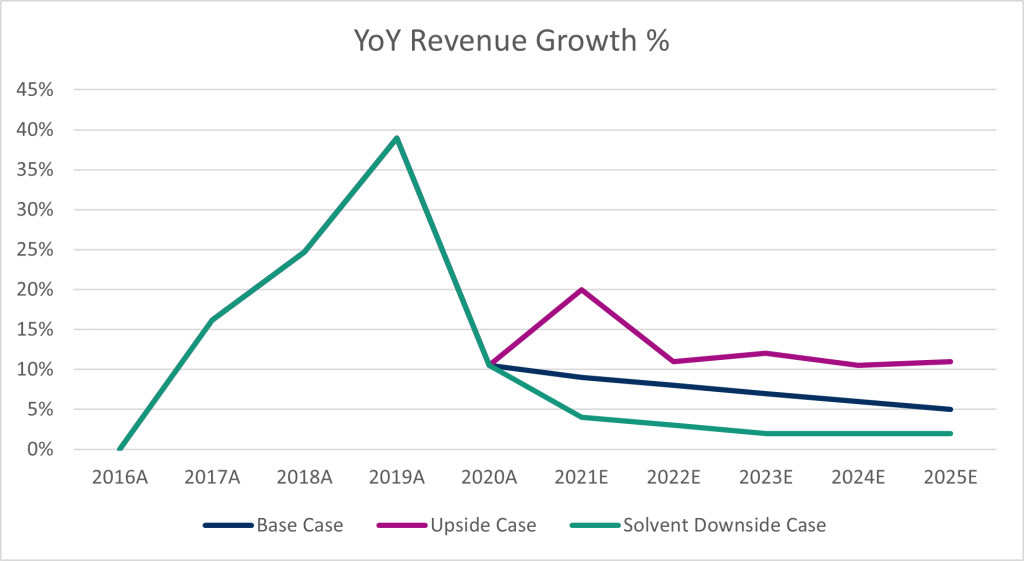

In terms of revenue forecasts shown above, my first action was to put together a regression analysis using the historical data I had to hand, which resulted in the following strong relationship between the previous year's Total Capital (i.e. Equity + Debt) and Revenue.

This actually forms the basis of the Upside Case scenario, whereby the company continues to enjoy the rapid growth it has seen in the previous few years. This looked quite bullish to me, and noting that broker research is expecting high single digit growth in the next couple of years (https://www.anexo-group.com/content/investors/analyst-research), I concluded that it was sensible to use this as an upside scenario.

For the Base Case revenue growth is modelled as starting at 10% and trending down towards 5% over 5 years, reflecting challenge in continued increases in scale.

The downside scenario reflects a complete flatlining of revenue, trending towards inflationary growth of 2%.

I would note that, assuming no change in total addressable market, even in the upside scenario Anexo would only achieve a market share of approximately 4.6%, and therefore this growth does appear achievable.

In the terminal year growth of 2% has been assumed in each scenario.

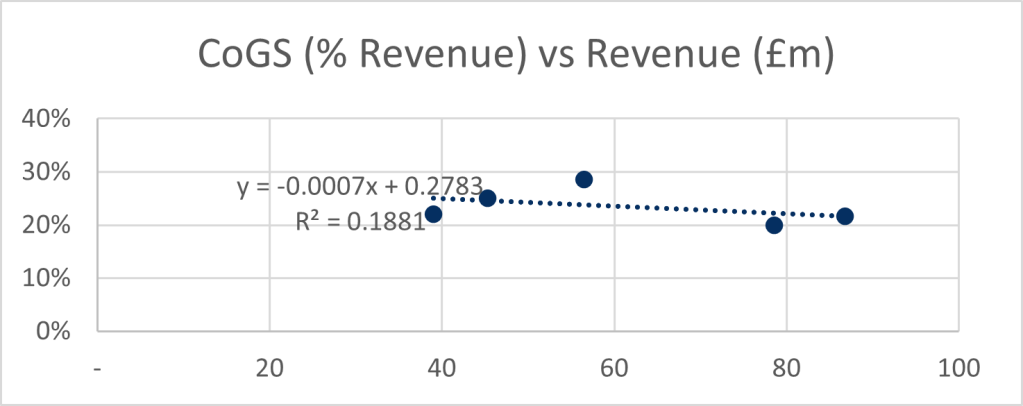

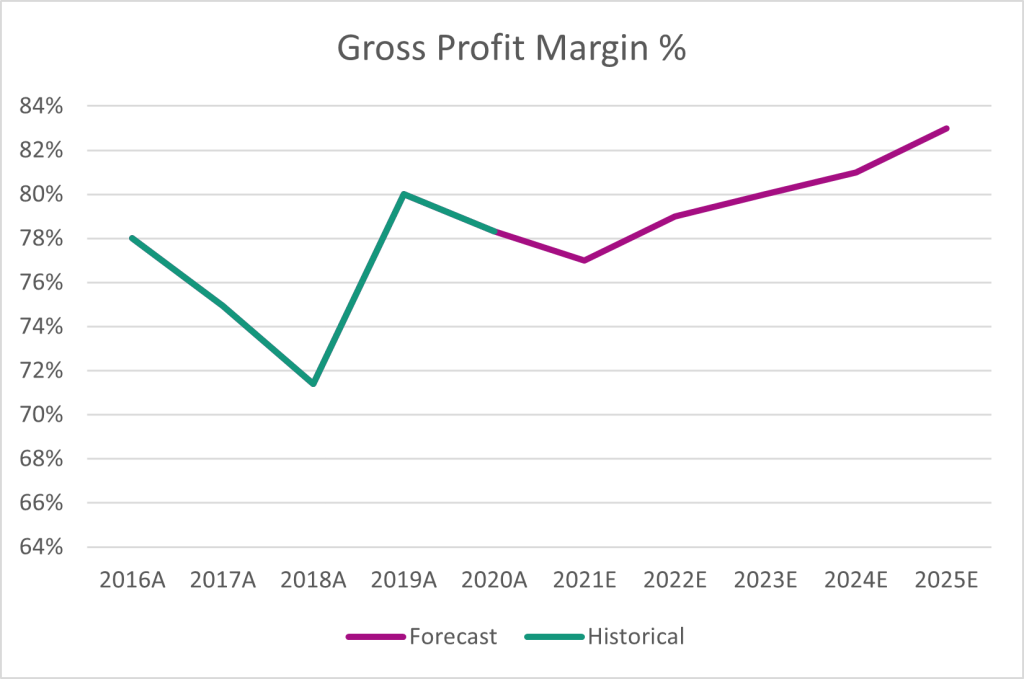

Gross Margin

Gross profit margin has been assumed to be constant across each scenario, primarily because the data is quite weak in terms of regression:

Though there is a weak correlation between GP margin and revenue, there is a slight trend downwards in CoGS (as % Revenue) and therefore a slight uptrend in GP margin which we might expect going to the future considering:

Anexo accepts approximately 50% of case applications, as time goes on and more experience is gained, accuracy of case selection should improve;

The large backlog in cases provides greater choice of cases from which a greater proportion should be successful.

Operating Expenses

Operating Expenses does show a strong relationship against revenue, reflecting the fact that much of the expenditure incurred by the company is variable.

This regression has therefore formed the basis of each scenario. I would note that in my forecasts I have used the revenue from 2 periods past to generate expected operating costs, the logic being that there will be some inflexibility over operating costs in the short-term.

CAPEX

Capex is only a small item in this business due to its nature, and for the purposes of the model I have used average CAPEX going forward, equalizing with depreciation in the terminal period.

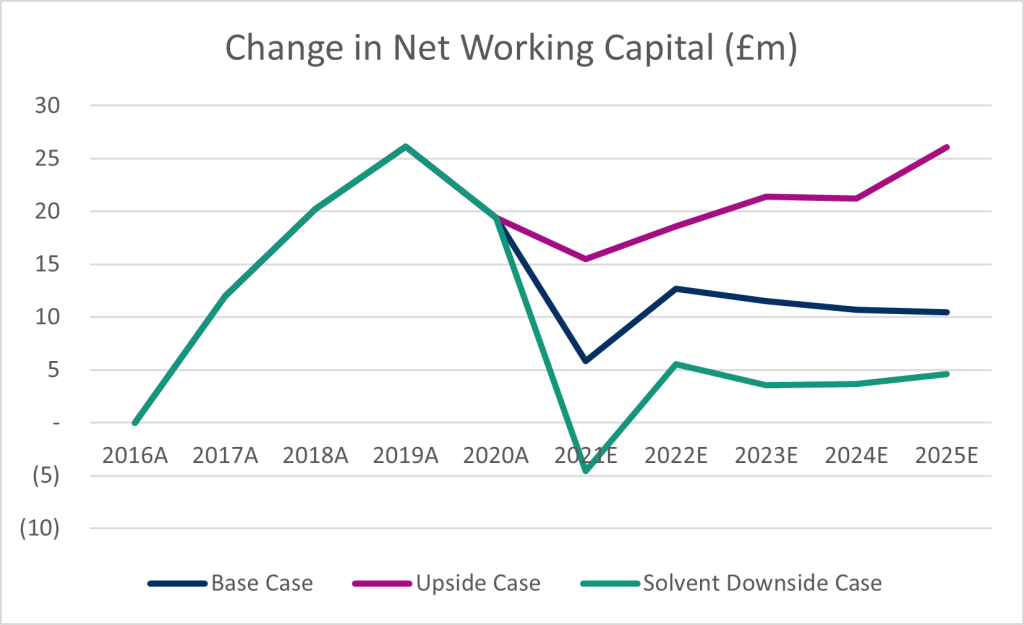

Working Capital

Because cases can take a year or two to come to their conclusion, there are high working capital demands on the business, as the business has to pay upfront for the replacement vehicles and the legal costs before making any recoveries.

A consequence of this is that in periods of rapid growth, the increases in net working capital will reduce cashflow generation in these years.

The following forecasts have been produced using the average Accounts Receivable, Payable, and Inventory days observed over the last 5 years.

The good news is that once this acceleration eases down to a steady state, there will not be such a demand for further working capital, which is reflected in the terminal year mid case cashflows shown below.

Beyond FY26 cashflows I have calculated a terminal value based on the Gordon Growth Model with terminal growth of 2%, in line with UK target inflation, which therefore (conservatively) assumes that no further market share can be gained after the forecast period.

WACC

I’ve estimate Ke at between 11% - 13% using the CAPM model, considering observed betas across the market, though this is difficult with highly limited available peers. I’ve also included a considerable small cap premium considering that this is small cap.

Cost of debt applied is 4% which is broadly consistent with the rate of 3.75% above LIBOR disclosed in the 2019 financial statements.

Calculated WACC applied is between 9.0% and 10.0%, which feels reasonable for me personally.

This has been used to discount expected free cashflow to the firm before the application of the Gordon Growth Model at 2% terminal growth as noted.

The resultant calculation gives an equity value range of between £230m and £196m, or between £1.70 and £2.00 per share, significantly higher than the current price level of £1.34 per share.

This results in an implied current year EV/EBIT of between 12x to 14x, reflecting the modest level of growth which is expected, this is as compared to a 10x multiple implied by the current share price. I would normally seek to compare multiples with peers, but there simply isn’t any sufficiently comparable listed companies out there.

Conclusion

Overall in my opinion Anexo Group Plc represents great value at the current price, which I think is what has been recognized by Dbay in their takeover interest. It also has the added bonus of offering genuine diversification with other assets in my portfolio and with the wider economy.

Target price: £1.85. Conclusion: doubled down at £1.34.