(POSITION CLOSED) BOUGHT: Argentex Group Plc – genuine multibagger.

(POSITION CLOSED) BOUGHT: Argentex Group Plc – genuine multibagger.

EDIT: position closed 01/12/2022 @118p, 59.5% total return, 107.8% annualised

Disclosure: I hold a long position in AGFX.

I’ve been a shareholder in Argentex Group Plc, a no-risk FX broker, for about 1 month. Today, I added to my position following a drop in share price. It has no debt, 26.6% 5Yr Historical CAGR, >20% ROIC, and has market price at 4.2x EV/NTM EBIT. This is the best value opportunity I’ve seen in 2022 so far.

The business model

AGFX is a no-risk FX broker who provide FX instrument solutions for non-speculative clients. In plain English, the company arranges FX contracts for businesses, who need them for their own risk management purposes (as opposed to speculative purposes), and it avoids taking on any proprietary position in FX instruments.

To take a simple example, Company A might be based in the UK but have a large customer based in the USA. Company A is exposed to currency risk because it sells its goods/services to this customer in US Dollars, and therefore the value of its revenue from this customer in GBP is subject to the FX rate. To avoid any cuts and scrapes from movements in currency, Company A could use AGFX to enter into an instrument to mitigate this risk. This could be an GBP/USD FX swap, a forward contract, or an option, but the end goal is the same. AGFX will match this contract back-to-back with a high credit quality financial institution, and therefore doesn’t carry any risk associated with the contract themselves, besides counterparty credit risk.

The business model is beautifully simple, and that makes it easy to understand the drivers of its success. What volume of contracts can AGFX maintain, can it maintain a low level of counterparty credit risk, and can it keep its operating costs down?

Volatility & economic environment

There are two competing forces at work when we consider the economics & cyclicality of the business.

On the one hand we have volatility. In a more volatile currency environment, the risk for businesses becomes larger and the benefit of FX hedging is greater, which plays in AGFX’s favor. I personally believe this effect to be overstated, because large corporates tend to engage in FX hedging habitually.

The other side of the coin is related to the amount of economic activity. If economic activity is subdued, which goes hand in hand with ‘economic uncertainty’, then the need for FX hedging on commercial transactions is also subdued, which explains the lack of revenue growth in the year ended 31.03.2021 following the pandemic.

There is also a fringe risk to consider, which is counterparty credit risk. If counterparties default on the obligations associated with their FX derivatives, then AGFX will be exposed. The company continually emphasizes using blue chip counterparties to back transactions and implementing strict take-on/KYC procedures with respect to clients to minimize this risk. This is in addition to avoiding speculative clients altogether. Regardless, in a severe economic downturn (think GFC style catastrophe), this becomes a more material risk.

Customer service and expertise

The competitive advantage for AGFX is customer service and expertise. Ultimately, it’s the relationships which the company builds with corporates which is fundamental to continuing to grow revenue, which in turn are founded upon the expertise and quality of service provided by the company. This is difficult to ascertain when the customer base is corporate, we can at least see from customer numbers available that churn remains relatively low, with a spike in 2021 financial year which we could put down to COVID to some extent:

Manager owned

I am always at pains to point out when management have a significant shareholding in the business, because skin in the game for them puts my mind at ease that we’re all in the same boat. Tick.

Quality fundamentals to date

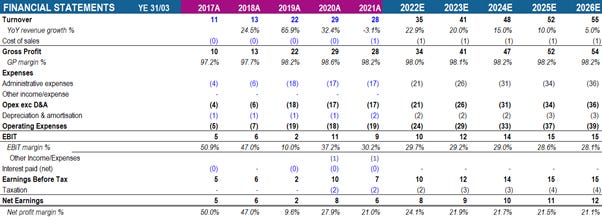

The trading update issued today had revenue (and earnings) at slightly below expectations (2022E below reflects todays announcement). I believe that the market overreacted to this, but in any case, the fundamentals remain strong with EBIT margins maintained around 30%, ROIC in excess of 20%, and CAGR over the 5 year period to 2022 at over 26%.

Model forecasts & DCF

Forecasts

In my forecasts I’ve conservatively assumed that margins will continue to decline (which I believe is reasonable given inflationary pressure on costs and lack of evidence of operational leverage to date). I’ve also assumed that revenue growth will taper off over the coming years, this is despite plans for expansion into Australia and The Netherlands moving along nicely.

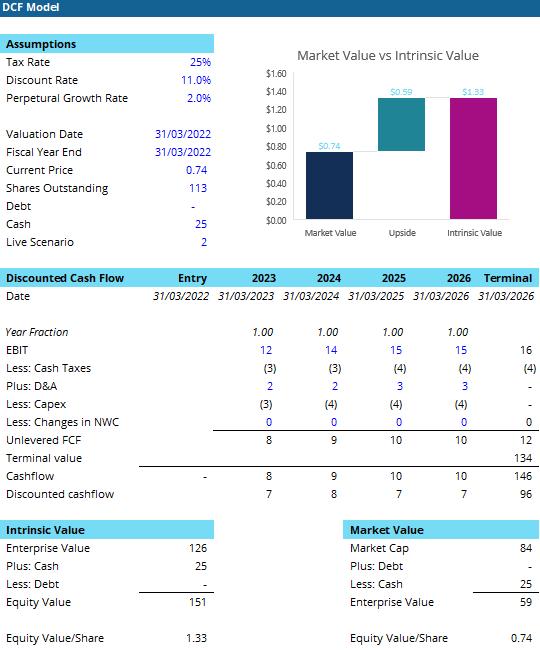

Beyond FY26 cashflows I have calculated a terminal value based on the Gordon Growth Method with terminal growth of 2%, in line with UK target inflation, which therefore (conservatively) assumes that no further market share can be gained after the forecast period.

WACC

I’ve estimate Ke at between 10% - 12% using the CAPM model, considering observed betas across the market, though this is difficult with highly limited available peers. I’ve also included a considerable small cap premium considering that this is small cap.

If it were not for the indirect exposure to cyclicality, I would suggest that this discount rate is a little on the high side, especially considering that the betas are completed unlevered.

Cost of debt is irrelevant as the company remains debt free.

Calculated WACC applied is between 10% and 12% therefore, which feels reasonable for me personally.

Model

I’ve assumed the Capex in the business will scale up with revenue, and working capital is negligible so nothing to worry about there.

The resultant calculation gives an equity value range of between £138m and £167m, or between £1.22 and £1.47 per share, significantly higher than the current price level of £0.74 per share.

This results in an implied current year EV/EBIT of between 9x to 12x, which I still feel is low balling it, but truly shows the value potential here.

Conclusion

Overall, in my opinion, AGFX is being misunderstood by the market in both its risk profile and earnings potential. Conclusion: doubled down at 74p. 1 year target price: £1.50.