BOUGHT: Creightons Plc – Growth Potential At A Value Price

BOUGHT: Creightons Plc – Growth Potential At A Value Price

Disclosure: I hold a long position in Creightons Plc

Last week I bought more shares in Creightons Plc, a business which manufactures and markets personal care and beauty products, which is based in the UK. In this piece, I explain why.

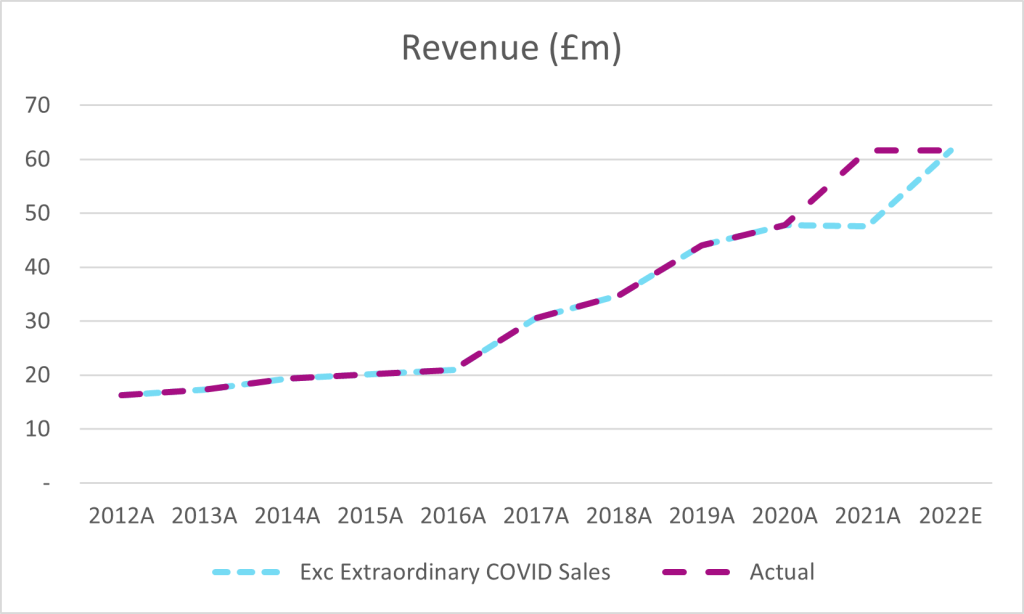

Creightons had been a beneficiary of temporarily heightened demand for COVID related hygiene products, adding £14m in extra revenue in FY21 to be exact, which caused a significant increase in share price initially, rising to over £1.50 per share. In FY22 the demand for hygiene products has become virtually non-existent, and on the realization of this and the fact that revenue and earnings will not grow in FY22, the share price promptly declined to where it is currently at 64p.

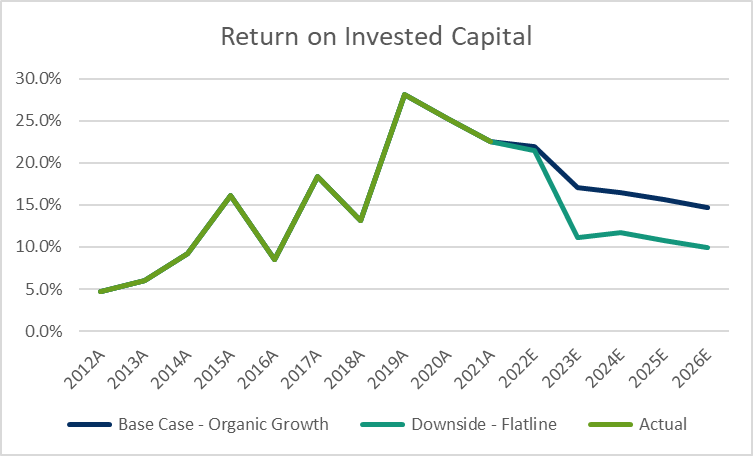

The basic premise of my argument on this stock is that the trajectory of revenue and earnings is being framed in the wrong way as a result of the extraordinary COVID-19 sales. The valuation of the stock at this level would look reasonable if you assumed that revenue growth will stagnate at 2% into the future and ROIC falls to around the WACC within the next few years. To put this into context, the company achieved a CAGR of c.23% in the 4 years prior to the pandemic and achieved an average of ROIC of >20% in the same period.

Despite the company losing out on c.£14m in revenue from the COVID sales, the company looks set to come out of FY22 with a similar level of revenue and earnings as in FY21, almost replacing the entire shortfall in sales through its core business. If we ignore the COVID-19 related sales figures, as is shown in the blue line below, it paints a picture of continued revenue growth through the COVID period, as opposed to flatlining purple line which is, in my view, the wrong way to look at it.

If revenue in H2 this year comes out as expected, this would represent a 5-year CAGR of 15%, and a ROIC in FY22 in the region of 20%, but the current share price is assuming a 2%-3% revenue growth and ROIC declining to 10% within the next 5 years. Under a base case scenario, assuming organic growth where a similar level of ROIC and growth is achieved, I estimate the fair value of the stock at 30% - 65% above the current level. Ultimately, this share price offers the potential of a growth stock at the valuation of a value stock.

Key risks and considerations

Inflation and margin stability

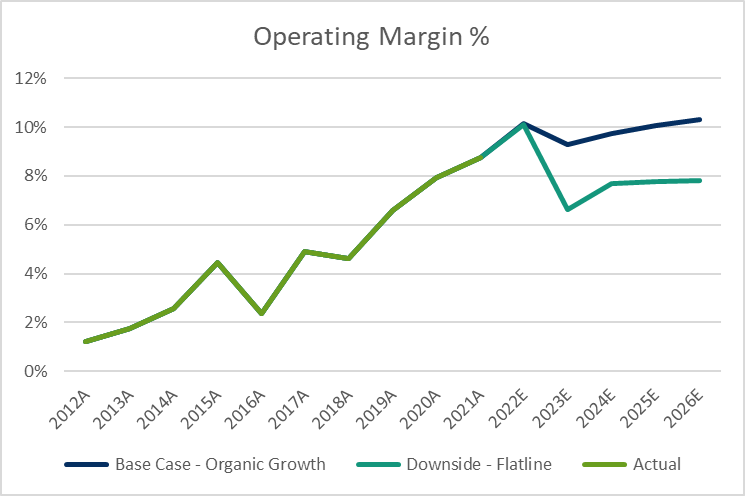

In todays inflationary environment, the robustness of margins should be at the front of every investors mind. Although operating margins have been increasing steadily at Creightons over the years, it’s ability to maintain these margins in an inflationary environment is unproven, and this presents risk.

The Creightons business model involves partnering with retailers to provide a route to consumers. These retailers, particularly larger ones, have significant pricing power and it remains to be seen if a higher cost base can be passed onwards. This point is particularly pertinent to discount retailers, like Superdrug, where price sensitivity is particularly high. Some comfort can be taken from the company’s current strategy of expansion into higher end product ranges, such as the Emma Hardie brand which was acquired during the year, where margins are naturally higher and where consumers are likely to be less price sensitive.

M&A and possible equity raises

A key part of the growth strategy of Creightons is the acquisition of new brands and businesses. The company used its strong cash position to acquire Emma Hardie and Brodie + Stone in 2021, which is a key reason why the business looks able to completely close the ‘hygiene gap’ left by temporary COVID sales in only 1 year, however it has been clear in recent updates that equity raises may be needed to fulfil the groups growth ambitions.

The business has said that it would provide it’s retail investors with the opportunity to participate in a future equity raise, which should guard against any risk of a cheap raise for institutional shareholders diluting shareholder value.

In 2021 the business appointed Gary Armstrong as Head of Business Strategy with the intention of accelerating the growth of the business through M&A. Gary does appear well qualified for the role: https://uk.linkedin.com/in/gary-armstrong-901a7550, which gives me some confidence, but it is hard to tell how successful the execution of the strategy will be. This a key point for investors, because how accretive the coming acquisitions are will be pivotal to value creation for shareholders.

For the avoidance of doubt, my valuation is based on a conservative estimate of organic growth only. The implementation of equity raises and the M&A strategy greatly increases the variability in outcomes for current shareholders.

Management ownership

Management own a significant proportion of the business, which is a significant positive, as there should be no doubt that the management teams interest are well aligned to those of the shareholders.

DCF Valuation

My valuation is based on relatively prudent forecasts of revenue growth, coupled with the operating margins noted above, and assuming no M&A fueled growth which could massively increase shareholder value.

I have valued the business based on the following 2 scenario, with probability weightings:

1. Base Case – Organic Growth (assigned 66% weighting)

2. Downside Case – Flatline (assigned 33% weighting)

For each of these scenarios, I have built separate DCF with differing assumptions.

Beyond FY26 cashflows I have calculated a terminal value based on the Gordon Growth Model with terminal growth of 2%, in line with UK target inflation, which therefore (conservatively) assumes that no further market share can be gained after the forecast period.

WACC

I’ve estimate Ke at between 10% - 12% using the CAPM model, considering observed betas across the market, though this is difficult with highly limited available peers. I’ve also included a 2.5% small cap premium considering that this is small cap.

Cost of debt applied is 3% to 3.5% which is broadly consistent with the rate of 3.04% secured loan the company has which is due to expiry in 8 years.

Calculated WACC applied is between 8.5% and 10.0%, which feels conservative for me personally.

This has been used to discount expected free cashflow to the firm before the application of the Gordon Growth Model at 2% terminal growth as noted.

The resultant calculation gives an equity value range of between £58m and £74m, or between £0.84 and £1.05 per share, including the 33% weighting to the downside case. This is significantly higher than the current price level of £0.64 per share.

This results in an implied current year EV/EBIT of between 9.0x and 11.3x, reflecting the modest level of growth I have assumed, this is as compared to a 7.6x multiple implied by the current share price.

Conclusion

Overall, in my opinion Creigtons Plc represents great value at the current price, even ignoring the large potential for upside should the M&A growth strategy be executed effectively.

1yr target price: £1.04. Conclusion: bought.