(POSITION CLOSED) BOUGHT: DNA 3 Ltd –Airlines Recovery Play (13% - 38% implied return)

(POSITION CLOSED) BOUGHT: DNA 3 Ltd –Airlines Recovery Play (13% - 38% implied return)

EDIT: position closed 16/01/2023 @57.535p, +72.2% total return, +75.5% annualised

Disclosure: I hold a long position in DNA3.

Preference shares over an airplane leasing SPV. Yes, I know what you’re probably thinking, but worthless junk bonds these are not. Assuming the latest aircraft valuation holds up (Mar 21), these preference shares have an implied yield of 37.8%. Hell, a 75% haircut on the aircraft valuation results in a yield of 13.4%. There are 3 key factors I believe make this a winner:

The key issue seems to be the value of these planes at the end of the lease, but even applying conservative estimates show a strong return;

There is still 3 years until the leases lapse, plenty of time for COVID recovery in the industry to work its magic on plane valuations;

The sole lessee is Emirates, who are backed by the government of Dubai. Emirates have a 100% payment record and the yield on debt instruments issued by Emirates show no signs of deterioration in credit quality.

Doric Nimrod Aircraft 3 Ltd (“DNA 3”) is an investment vehicle set up in 2013 for the sole purpose of purchasing A380 airplanes and leasing them to Emirates to earn a return. They purchased 4 A380 aircraft using debt and preference share equity, and then leased these aircraft to Emirates on a 12-year lease. The preference shares were issued at par with an annual coupon of 8.25% paid quarterly, the idea being that the payments from the lease match against repayments on the debt, and the dividend on the preference shares. To date all dividends of 2.0625p continue to be made on the shares which trade currently at 37p.

The return for holders of the preference shares is twofold. Firstly, the payment of dividend itself. Secondly, at the end of the leases whatever capital which arises from the disposal of the aircraft will be returned to the shareholders.

So, when assessing if this is in fact a good opportunity, let’s think about both in turn.

Dividend Payments

The reality with the dividend payments is that Emirates is a good quality borrower, as shown by current yields on it’s debt instruments:

“As at the end of December 2021, Emirates has outstanding USD debt issuances with maturities in 2023, 2025, and 2028. These respective bonds were all trading at above par (100 cents) and with running yields ranging from approximately 3.8% to 4.4% in USD. There has also been no upward pressure on yields. This level of yields does not appear to indicate any significant financial stress to the issuer.”

Latest quarterly factsheet: https://www.rns-pdf.londonstockexchange.com/rns/4003Y_1-2022-1-13.pdf

Emirates haven’t missed any payments, and financials have recovered significantly since 2020. Still, if there is some doubt over their credit quality, comfort should be taken from the fact that they remain supported by the Government of Dubai:

“In the first half of the 2021/22 financial year, the carrier’s ultimate shareholder, the Government of Dubai, injected a further AED 2.5 billion (USD 681 million) into the Emirates Group by way of an equity investment, demonstrating continued support for the airline on its recovery path.”

I can’t see Dubai contemplating the PR shitstorm which would ensue if Emirates were to default on it's obligations. Truly, I think the lease side of things is not the key worry here. What will really be the determining factor in this investment case is the outcome at the end of the lease.

End of Lease Return of Capital

Turning our attention to the second part of the return, the sale of the Aircraft. Now then, I can’t say that I know the first thing about the value of aircraft, let alone that I am an expect. But we can at least examine the facts. In each quarterly factsheet produced by the directors, an update is provided as to the valuation of the aircraft and hence the possible return of capital to shareholders at the end of the lease.

Since March 2020, the directors have been applying “soft values” to aircraft to account for COVID impact. As per the December 2021 release:

“The Directors note that the outlook for the A380, and hence the total return of an investment into the Group, is subject to an increased amount of uncertainty. From the outset of the transaction, the Directors relied on appraisers’ valuations based on the assumption that there would be a balanced market, where supply and demand for the A380 are in equilibrium. These values are called future base values. At the instruction of the Group this assumption was changed for the March 2020 appraisals onward. Appraisers assumed a soft market, characterized by less favourable market conditions for the seller, including but not limited to an imbalance of supply and demand in the aircraft type.”

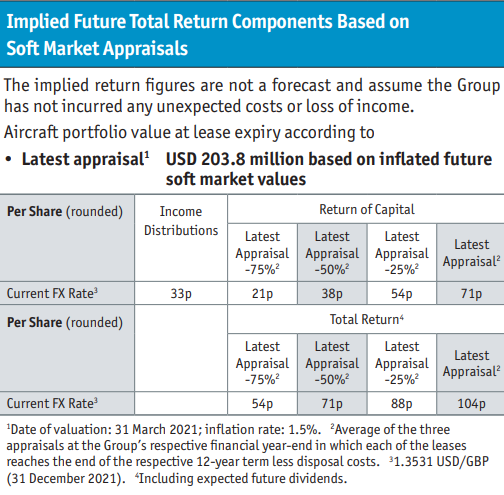

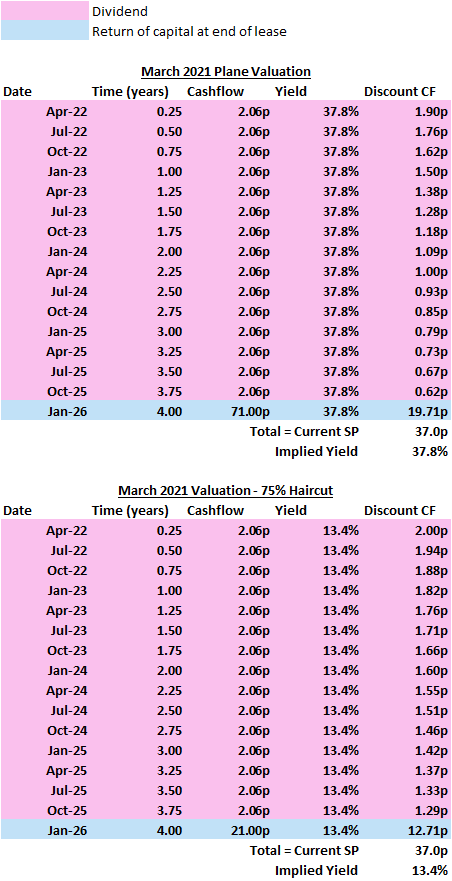

So, let’s be clear, dampened down valuation are already being applied when these disclosures are made. Even so, under the March 2021 valuation, the directors note that a return of capital of 71p per share should be possible, nearly double the current share price. As we shall see, even a drastic 75% reduction on the valuation amount results in strong returns for the preference shares at these prices.

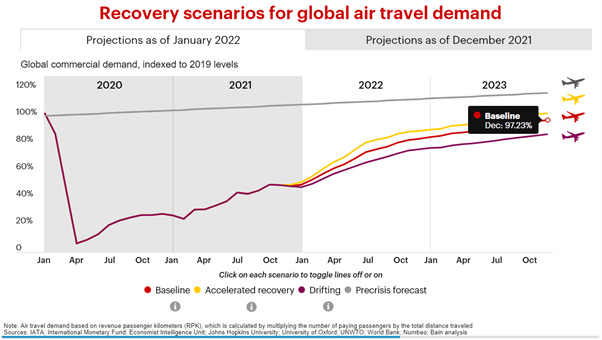

Beyond this, I think there is a lot of room for further upside. The ultimate concern here is that the supply of aircraft will far outstrip the demand, because the demand for air travel is currently still badly hit by COVID. While it is true that airlines have been heavily hit by COVID, it is also true that the prospects for the industry have never been better since COVID-19 began. The following scenarios I’ve pinched from Bain & Co (https://www.bain.com/insights/air-travel-forecast-when-will-airlines-recover-from-covid-19-interactive/) see global air travel returning to 97% of the pre-COVID level by 2023.

The leases on the A380 which DNA3 leases aren’t up till the end of 2025. With the milder Omicron variant becoming the dominant strain of COVID, it is my view that the time up to 2025 is by far long enough to see this recovery play out and hopefully this will mean that demand for A380s will allow for a decent realizable value. Moreover, I’d also consider the upside in the fact that the planes have been parked for much of the pandemic. Less mileage ought to mean better condition planes, and better returns.

Implied Yields

The following tables speak for themselves, the top one shows a favourable outcome, but still using the dampened down valuations. If the latest valuation is achieved, the implied return on these shares is 38% (as shown in the top table). Even if we take a 75% haircut on this valuation (the bottom table), the implied return is still 13%. Considering that these shares were initially issued at an 8.25% yield, I believe this presents very good value.

Somehow, I just can’t shake the feeling that something’s up, is something here too good to be true? Let me know what you think. For me, I can’t see how the risk associated with this is so high to justify yields of this size. Conclusion: BOUGHT at 37.0p.