(POSITION CLOSED) BOUGHT: London Security Plc – Defensive Pick With 20 Years Consistent Performance

(POSITION CLOSED) BOUGHT: London Security Plc – Defensive Pick With 20 Years Consistent Performance

EDIT: position closed 28/02/22 @2,900p, +25.6% total return, +47.9% annualised

Every now and again my feelings of paranoia regarding the bubbliness of equity markets flares up, and so I’ve recently been looking for something to add to my portfolio which might provide some protection in a recession situation. This week, I’ve added London Security Plc (AIM:LSC) to my portfolio, a leading fire protection company with 200,000 customers across Europe.

The company sells fire protection equipment outright, and earns fees through the installation, maintenance & servicing of equipment. The business model is therefore very easy to get your head around and, crucially, the product offered is essential, allowing for protection in a downturn (see performance through 2008 GFC). It’s also boring, which works for me.

I’ll get into the detail, but to summarize why I’m excited about this stock:

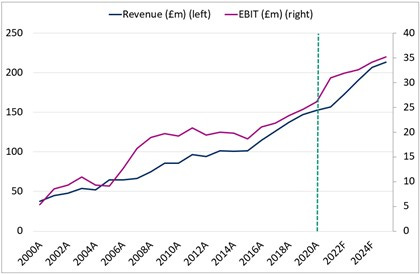

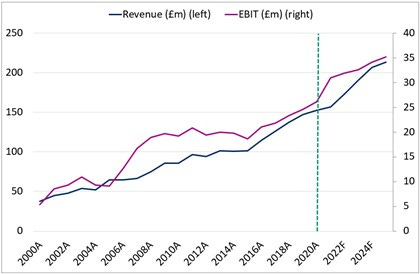

Average 5yr CAGR since 2005 – 2020 of 6.8%, remaining profitable throughout 2008 GFC;

EV/LTM EBIT < 10x;

20% - 45% undervalued;

Unlevered FCF margin of 12% from 2000 – 2020, with only one year of negative (2008: -0.8% margin)

Positive net cash position as at 31/12/2020 of over £30m;

98% owned by the Chairman;

Small free float means this stock has very little coverage.

The key risks facing a potential investors are in my opinion:

Margin pressure from competitive market;

Continued growth relies on acquisition strategy;

Low liquidity – higher broker spreads volumes only suitable for small portfolios

Under the radar

Usual issues with low liquidity stocks include the small size of capitalization, businesses which are not well proven or might not be well established, and businesses where there is a general lack of information. This stock however doesn’t have any of these issues, the company has market capitalization of c.£300m and only has low liquidity because the free float is <2% (with the chairman holding the vast majority of shares). It has a long track record for all to see, but the low level of liquidity means that this stock is only a viable investment for private investors, and nobody has ever heard of it. There simply isn’t enough stock for any institutional investors to even look into this, and as a consequence there is next to zero coverage of it.

This is why I think this opportunity has flown under the radar, and although there are some downsides to owning something with such low volumes (it took me a few days to have my order filled), it provides genuine unexplored territory for retail investors to capitalize on.

The reason the company has such a small portion of shares in the public domain dates back to the 1990s. The company dates back to before 1900, but in 1992 the company (as it existed then) ran into financial difficulties and, to cut a long story short, shareholder dilution and several share buyback programs has resulted in the small public ownership of today. The company as it exists today comprises a large number of different brands in the UK, Belgium, Austria, The Netherlands, Luxembourg, Denmark, Germany, and France, and has built consistent performance over the last 2 decades.

Management owned with excellent track record

Personally it makes me feel at ease when those involved with running a company have themselves skin in the game. Jacques Gaston Murray is the Chairman and largest shareholder of the company and has been involved with the company for many decades, with other family members serving on the board: https://www.londonsecurity.org/about-us/board-directors.

This is a big plus for me, but the biggest attraction of LSC is its track record has been used to form the basis of my valuation model…

Good pricing with margin of safety

DCF Model

In order to value the company, I have put together a standard DCF model based on enterprise level cashflows, based on my view of a mid case.

Revenue forecasts are based on a regression analysis which assumes the company is able to continue to grow through acquisitions as it has consistently done over the past 20 years.

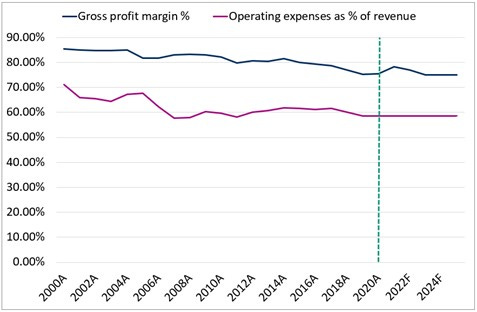

Gross profit margin is assumed to continue its decline reflecting continued pressure which is shown in the graph below. This pressure has in the past been somewhat offset by a more efficient cost base, shown below by a reduction in operating costs as a proportion of revenue. As a conservative assumption, this has been assumed to remain flat over the forecast period.

Incremental increases in net working capital have been factored into the cashflow, which are relatively minimal. Maintenance capital expenditure has been regressed against revenue and factored into cashflows.

Beyond FY25 cashflows I have calculated a terminal value based on the Gordon Growth Model with terminal growth of 2%, in line with UK target inflation, which therefore (conservatively) assumes that no further market share can be gained after the forecast period.

I’ve estimate Ke at between 8% - 9.5% using the CAPM model, considering observed betas across the market, though this is difficult with highly limited available peers. I’ve also included a considerable small cap premium which is debatable especially considering the valuation is compared against the ask price below.

Calculated WACC applied is between 7.5% and 8.5%, this reflects the low volatility and the essential nature of the product, and I’d note that the WACC disclosed in the annual report of c. 10% (pre-tax) is broadly consistent with this.

This has been used to discount expected free cashflow to the firm before the application of the Gordon Growth Model at 2% terminal growth as noted.

Noting that the company is in a net cash position of c.£30m, the resultant calculation gives an equity value per share range of between £29 and £34, providing >20% margin of safety above the current ask price of £23.4.

Multiples

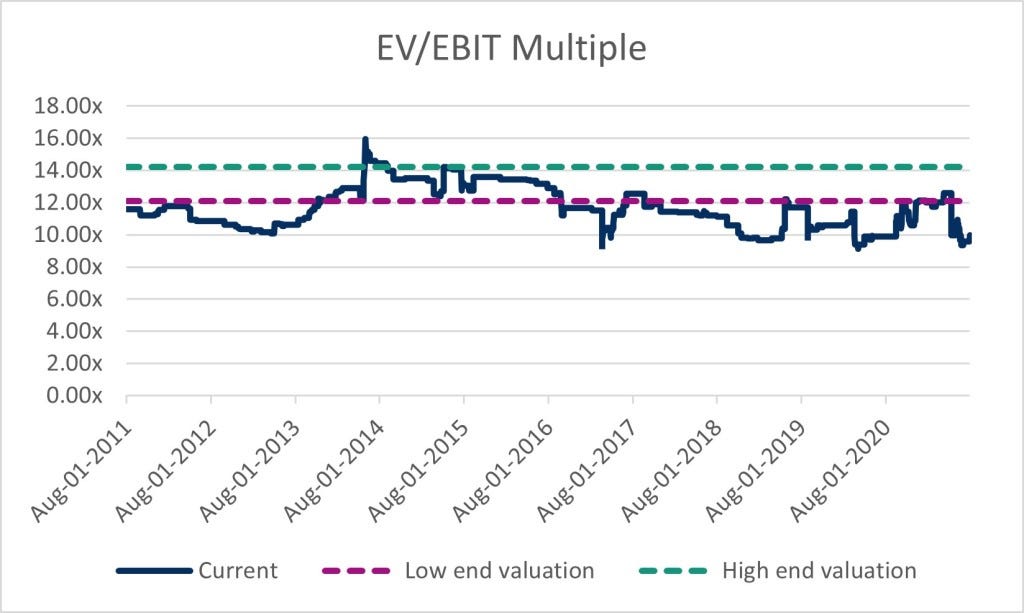

This results in an implied current year EV/EBIT of between 12x to 14x, reflecting the relatively mature business which LSC is. There is very little in the way of peers from which to compare, however we can see that this valuation is broadly consistent with capitalization over the last 10 years. The current multiple of below 10x is as low as it has been over this period.

Conclusion

It is very rare to find a company with such a long and consistent track record as this one, even more so for a company of this size. Overall London Security Plc represents a little known opportunity, only available to small retail investors, to gain exposure to a management owned defensive stock, at an attractive price.

Target price: £31. Conclusion: bought at £23.40.