EV/EBIT Multiple Cheat Sheet

EV/EBIT Multiple Cheat Sheet

...USE THIS TO SCREEN YOUR STOCKS

Before you continue, I just want to thank all of you for your support. We all start somewhere, and every reader is well appreciated!

Do you ever look at share price multiples and think, is this good value, or just poor quality? Here’s a tool you can use to filter stocks out before diving in deeper.

Prior to building this tool, I had put together a model for a company I was interested in. I liked that it had little debt, it had a good track record, and it looked like a good price when I was relying on my intuition, and overall I thought I was on to a winner.

However, having put together a full DCF model, the price really didn't leave any margin of safety at all, and this was primarily down to the level of perceived risk and the resultant discount rate.

The lesson in this is that you always need to be looking at a full cashflow to really know where you stand, and for me it made it very clear that my intuitive perception of value is actually quite insensitive to the level of risk.

Off the back of this I was thinking to myself, I wish I had something which could help me to screen potential ideas a bit more effectively, so I decided to come up with a simplified 'cheat sheet' of multiples, not as a substitute for doing a full cashflow, but only to help with preliminary screening.

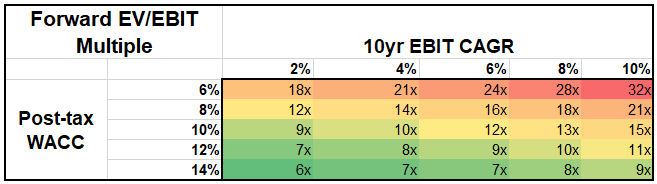

This table calculates the ‘fair value’ multiple using several simplifying assumptions noted above. Timing of cashflows and NWC profile may be sway this one way or another in practice, but it’s a good place to start.

The table basically sensitises the two basic inputs into valuation, risk and cashflows. As we all should know, it shows that risk needs to be in the front of the mind of the investor.

To take the example in question, my calculated post-tax WACC was around 11%/12%, consistent with what was in the accounts, and in my model the EV/EBIT multiple for year 2 was around 14x based on current market cap and book value of debt. With some growth but not rapid growth (CAGR from year 2 to year 10 at around 4%), the table would give a rough forward multiple of 8x-10x before NWC, with 14x appearing not crazy, but optimistic.

Do yourself a favour and ask yourself:

What would be a reasonable WACC for this investment

What annual growth in earnings can I expect over the next 10 years?

Is the corresponding multiple lower, or higher, than that implied by the current price?

If lower, move on. Better to screen opportunities with the table first, do a full cashflow second.

Thanks for reading

Eddie