MODEL UPDATE (free download): Anexo Group Plc

MODEL UPDATE (free download): Anexo Group Plc

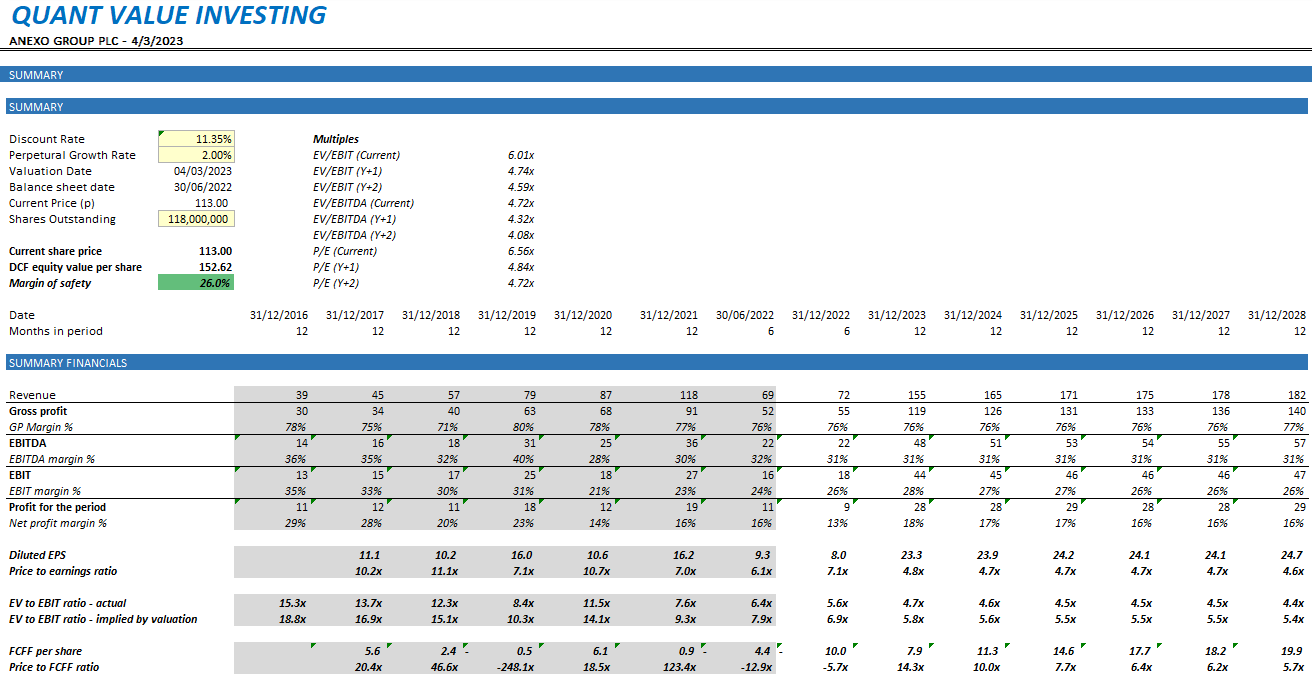

Key facts: 26% margin of safety, 6.01x EV/EBIT, 6.56x P/E, 0.96x P/B, 12.7% 5yr Avg ROIC

Model update key facts (free model download below):

Fair value estimate at 153p, giving margin of safety c.26%

WACC applied: 11.35%

EV/EBIT (CY): 6.01x

P/E (CY): 6.56x

P/B: 0.96x

12.7% 5yr avg. ROIC

Financials Summary

Want to apply different assumptions? Download the model for yourself!

Questions or comments?

Business background

UK company offering credit hire services & legal services to victims of non-fault vehicle accidents.

Key Advantages

The business performance has little correlation with the performance of the wider economy, offering genuine diversification;

The business has been growing at speed, with revenue growing at a CAGR of 25% over the last 5 years;

Management still has large % ownership in the business;

Market share increasing, but still currently only 3%, providing ample room for further expansion;

Low P/B ratio of 0.96x, which is due to large amount of working capital required in the business.

Key risks

The business model is underpinned by a ruling by the House of Lords whereby non-fault accident victims have the right to recover credit hire rates from third party insurers, there is therefore a key risk that further developments in case law disrupt the business;

Expansion into housing disrepair and vehicle emission less proven.

Detailed business model

The company, based in Liverpool in the UK, operates a business model whereby they assist in legal claims associated with non-fault vehicle accidents, and it specializes in impecunious legal claims. An impecunious claim in this context essentially means that the party making the claim does not have the financial means to source a replacement vehicle (think of the scenario in which a local tradesman gets into an accident, and can’t afford to purchase a replacement vehicle which they need in order to work).

The services offered by Anexo in this scenario are twofold: 1) Anexo will assist the claimant in sourcing a replacement vehicle via a credit agreement (this part of the business is called EDGE), and 2) Anexo will process the legal claim against the relevant insurance company to resolution (through its wholly-owned firm of solicitors Bond Turner). To illustrate, this diagram was provided in the Anexo year-end results:

Anexo charges fees associated with both the credit agreement in place with respect to the vehicle, and fees associated with processing the legal claim. The company operates on a “no win, no fee” basis, and therefore a key risk to the business is the success rate of legal claims undertaken. However, a good thing about this area of the legal sector is that the cases are high volume and low value, meaning the risk is well distributed and the cases are typically very standard in nature. As such the failure rate when cases go to trial is below 2% and in fact the vast majority of cases are settled before trial.

The main area of weakness that is inherent in the business model is its vulnerability to further changes in the law. The existence of the business is predicated on a series of House of Lords rulings which set precedents for what rights impecunious claimants have in a vehicle accident situation. Though the leading case with regards to this dates back to 2003 (Lagdan vs O’Connor, https://publications.parliament.uk/pa/ld200304/ldjudgmt/jd031204/lagden-1.htm), further developments continue to unfold (https://www.blmlaw.com/news/to-be-or-not-to-be-impecunious-that-is-the-question), and there is a risk that further developments significantly damage the ability of Anexo to earn revenue.