Not all banks are created equal: why I still own Secure Trust Bank (LSE:STB)

Not all banks are created equal: why I still own Secure Trust Bank (LSE:STB)

Key facts: >80% of customer deposits from fixed term bonds & notice accounts, 57% average loan to value on RE lending, margin of safety 45%, 3.25x P/E, 0.42x P/B, 10.3% 5yr avg. ROE

The last few weeks have not been pretty for the banking sector. The fall of Silicon Valley Bank & Signature Bank in the US followed by the Swiss central bank intervention to support Credit Suisse has sent shivers down the spines of investors. What was already an out-of-favour industry has gone from bad to worse, with some investors declaring banks in general outright uninvestable.

I think that, as with any all companies, it is crucial to understand how they actually function, and in particular understand what the risks are. Whilst it may be true that for some large financial organisations it is all but impossible to untangle the risks involved, simpler financial businesses exist where I believe this can be done.

Moreover, without sticking my neck out too far, there are idiosyncratic factors which apply to each of SVB, Signature Bank, and Credit Suisse which don’t necessarily apply to peers across the industry, and certainly not to Secure Trust Bank as we shall see.

SVB, Signature Bank, and Credit Suisse

Taking each of these in turn:

SVB - the failure of this trash bank resulted from a liquidity crisis, it could not meet depositors withdrawal requests, this happened because:

It invested a massive proportion of its assets in long-dated treasury bonds & mortgage backed securities whilst rates were at record lows, with no interest rate hedging. This left SVB with large unrealised losses as a result of rising treasury yields.

Large unrealised losses spooked depositors, primarily start-up businesses. The majority of depositors had a right to access cash on demand and were already prone to withdrawing plenty of cash over time, because burning cash is what start-ups do.

Signature Bank - this bank had similar failing to SVB, in terms of the kind of depositors it held. Add in to the mix large losses on crypto assets and this dumpster fire couldn’t handle the wave of withdrawals which followed the SVB collapse.

These two banks epitomise the excesses of the tech & crypto industries, and note that these failures didn’t come from credit related issues, which is not to say that there aren’t any, but instead came from reckless mismanagement of market & liquidity risks.

Credit Suisse - this piece of garbage has been involved in scandal after scandal, including but limited to:

Greensill collapse

Archegos collpase

Mozambique bribery scandal

‘Suisse secrets’ median investigation

Bermuda trial

Bulgarian cocaine network

Material weaknesses in internal controls

Need I continue? The demise of Credit Suisse has not been an abrupt spare of the moment event, it has been a slow-motion car crash all of it’s own making, from which we can make very few conclusions about other industry peers.

Not all banks are like this.

Secure Trust Bank Plc

Secure Trust Bank Plc (LSE:STB) is a straight-forward deposit taking lender, operating solely in the UK & headquartered in Solihull in the West Midlands, and is regulated by the FCA & PRA. The company was incorporated in 1954 and has a long track record in the industry. The company was listed on the AIM in 2011 but currently trades on the main LSE market.

Asset-side

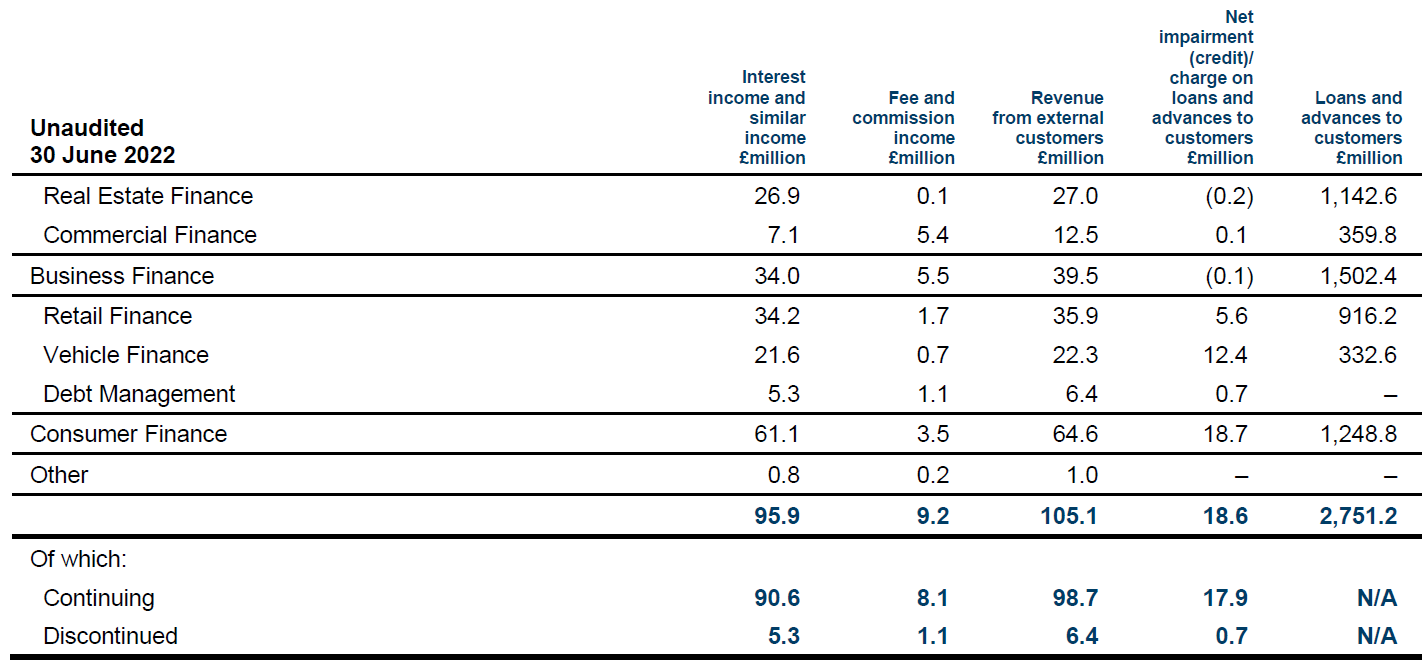

The company’s lending portfolio is split broadly equally between Consumer Finance and Business Finance portfolios, with the largest revenues being earned in the Retail Finance and Real Estate Finance segments.

In terms of credit quality the loan book shows no signs of deterioration, and the focus for the bank has been to target prime borrowers in specialised markets, allowing it to maintain margins without compromising on credit quality. I would also highlight again that whilst credit is a risk to keep an eye on going forwards, the frailties in the banking industry we have seen recently do not stem from credit quality issues.

The largest segment is Real Estate Finance. I do expect trouble ahead in this sector and by way of example I could point to Inland Homes Plc (LSE:INL), a developer which has been through difficulties lately, to whom the bank have a £26m exposure. However, it’s important to note that the bank only loans below 65% LTV for developers, below 70% for rental assets, and it has an average LTV of 57%. This gives significant headroom for recoveries should there be a downturn.

The second largest is Retail Finance, where again the focus for the bank is prime customers, and to date there has been no deterioration in credit quality.

It is worth highlighting that the banks mix of assets has a relatively short duration (e.g. retail finance), which gives it more protection against rate risk and liquidity risk as compared to most banks. This is because rates on assets reprice more quickly and should there be a sharp reduction in deposits, the banks shorter-duration assets will provide liquidity more quickly. Moreover it has no trading/investment book which limits it’s market risk. All of these factors were pivotal in the recent issues with SVB and signature Bank.

Deposit side

On the deposit side, Secure Trust Bank has a low reliance on wholesale funding and the vast majority of it’s deposit base is either in notice accounts and fixed term notice accounts, which unlike SVB or Signature Bank means it has better forward-looking visibility on liquidity and is better placed to manage this risk.

The risks in terms of deposits are there that there is an outflow over the coming years as the economy slows and large inflows from the COVID period reverse, and related to this that the cost of deposits rises steeply. Secure Trust Banks shorter duration asset base and high NIM profile should help it deal with this, however it’s loan to deposit ratio is already around 120% and it will need to act quickly should this materialise.

Despite this risk, deposits continued to grow up to the end of 2022 according to the banks pre-close trading statement.

Profitability

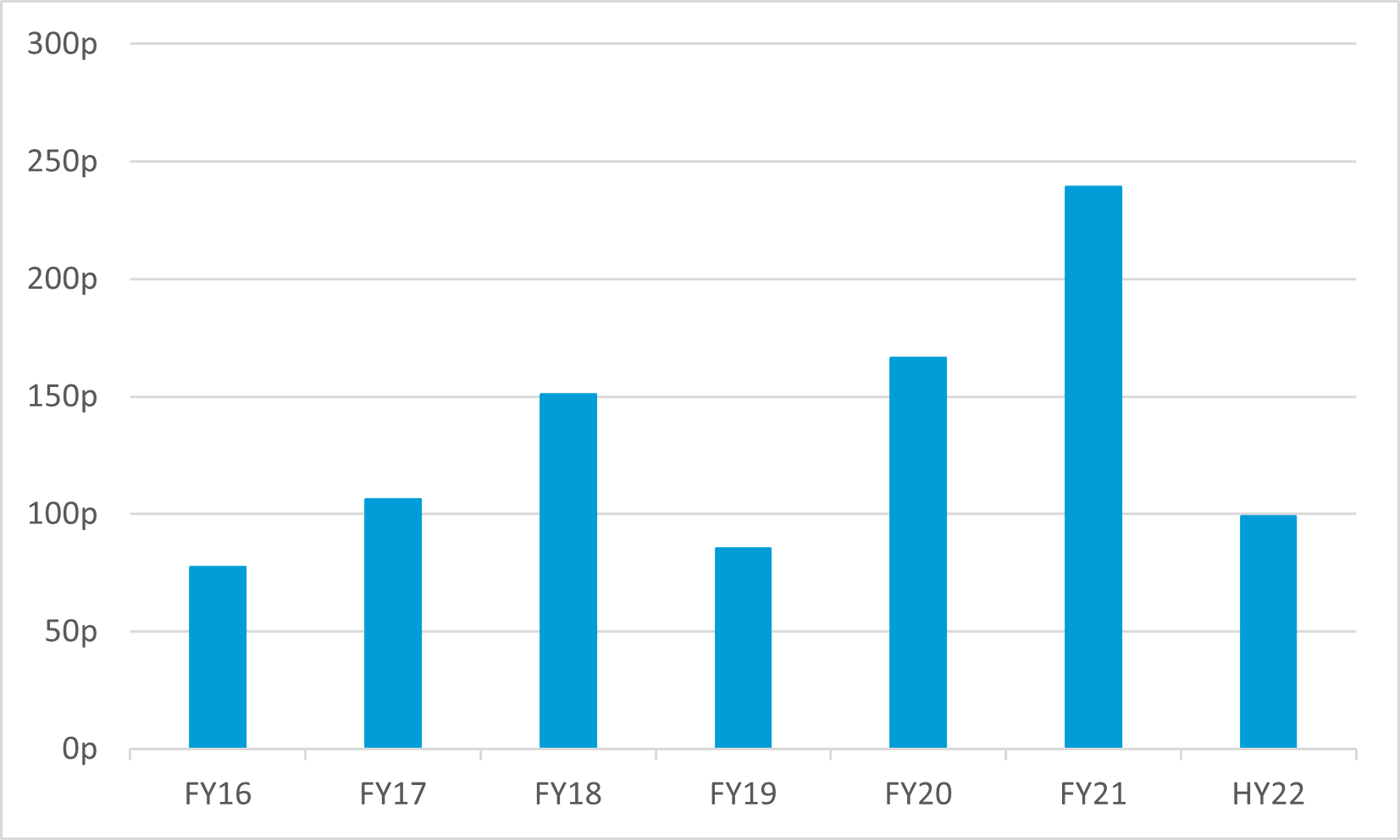

In the last few years the company has shown strong organic growth with EPS climbing from 77p per share in 2016 to over 200p in 2021 and likely 2022. This is despite a challenging interest rate environment for banks which has depressed valuations across the sector for years.

STB has focussed its strategy on higher yielding specialist lending coupled with a lower level of leverage on the balance sheet (i.e. with a higher ratio of capital to lending assets), which has allowed it to maintain a strong net interest margin which is far less sensitive to changes in interest rates as compared to lower yielding lending areas such as standard residential mortgages. This has allowed STB to increase its net interest & fee revenues before loan losses from £107m in 2016 to over £150m 2021, which has been achieved at the same time as pivoting it’s loan book towards higher quality assets.

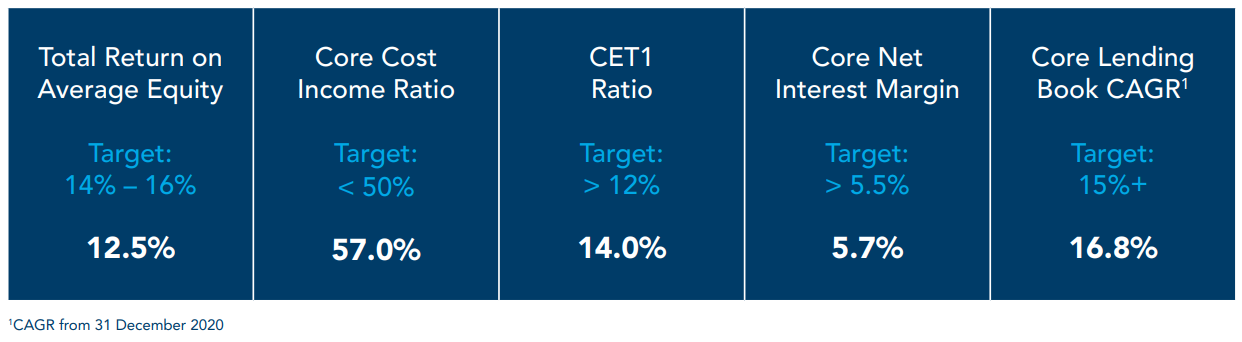

This level of profitability has meant return on equity in excess of 10% over this period, with the latest trading statement in January reaffirming strong profitability. The management team is targeting 15% ROE in the medium term. Whilst I think this is ambitious and I am more conservative in my valuation, what is clear is that the valuation implied by the share price assumes much lower return on equity than has historically been achieved.

Capital

Signature Bank and SVB have made a mockery of capital ratios in recent weeks, with capital ratios looking ok on paper, however these didn’t take account of mark to market losses on poor investments which has little application here. Over the last few years Secure Trust Bank has maintained a strong balance sheet position, exceeding minimum regulatory requirements throughout. As at 30 June 2022 the bank maintained a Tier 1 capital ratio of 14.0%.

Valuation

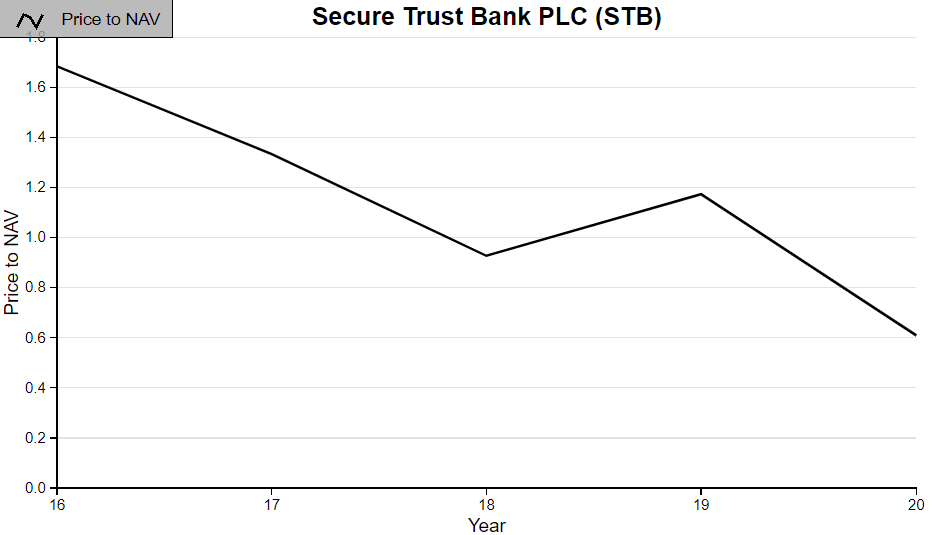

Despite coming through the COVID period unscathed & being profitable / maintaining good return on equity throughout, Secure Trust Bank is currently valued at an all time low in terms of earnings & book value. The current share price implies a P/B ratio of around 0.4x.

Baking in risks around credit deterioration and rising costs of deposits, I value the bank at around 1,300p (vs current price close to 700p), but I will release a full model update in the coming weeks once the full year results are announced at the end of the month.

Thank you for reading, your support goes a long way!

Eddie Lloyd