Royal Mail Group Plc (Free Downloadable DCF Model)

Royal Mail Group Plc (Free Downloadable DCF Model)

This weekend I was thinking of writing a research piece about Royal Mail Group Plc (LSE:RMG), currently priced at £4.62 per share at the date of publishing. It's a stock that I've been monitoring for a little while and, prior to making my mind up, I thought I'd build a basic model to see if it drew out any conclusions one way or the other.

By coincidence I read a great article by Phillip O’Sullivan covering this: https://tbifund.wordpress.com/2022/01/22/royal-mail-group-rmg-ln-delivering-returns/, and so I thought I'd save myself the trouble of writing up a complete deep dive.

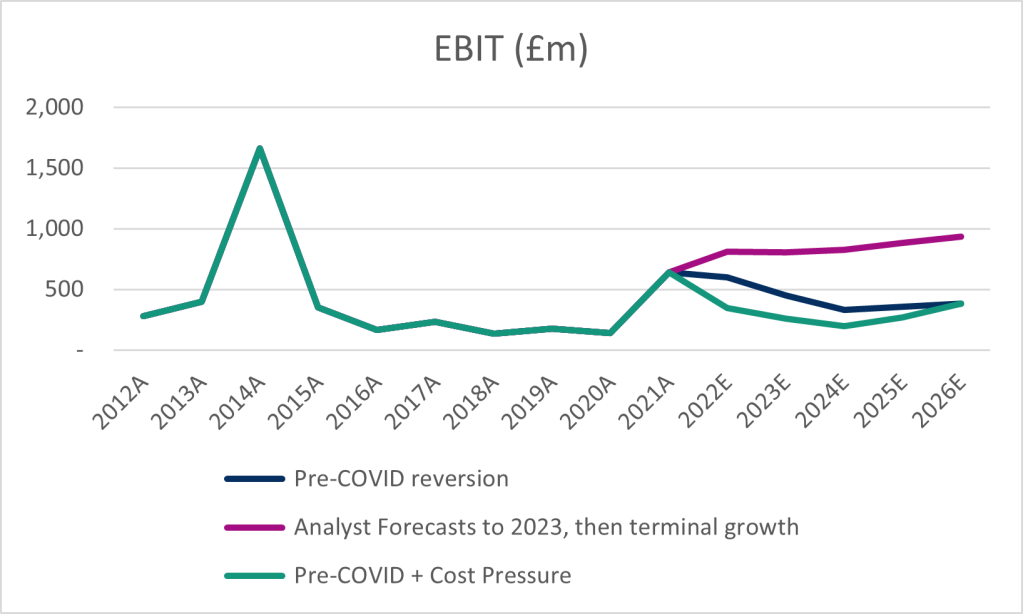

To summarise the basic position of the company: Royal Mail operates delivery services, primarily in the UK, but also across Europe. It has been a prime beneficiary of COVID in that delivery services have been in record demand, and this saw RMG achieve a strong EBIT of £640m in FY21, significantly higher than in previous years. This implies an EV/EBIT ratio of <8x, hence the potential opportunity.

In considering whether this is a worthwhile opportunity, there are some key risks to bear in mind:

Will the recent uplift in revenues be sustained into the future, or will it revert back in the next few years?

Can RMG maintain the current margin level, considering inflationary pressure? This may be a particularly pertinent issue for RMG with unionisation in its UK workforce being a high barrier to automation and cost control.

Does the supremacy of the likes of Amazon pose risk to RMG, which would otherwise be a relatively monopolistic business?

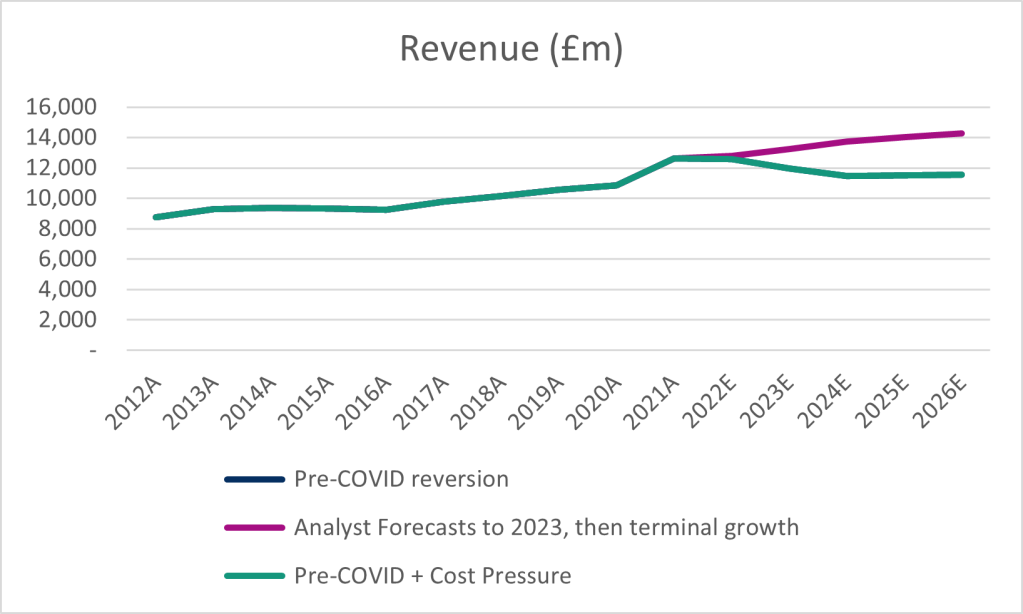

With this in mind, I've put together the following downloadable enterprise level DCF, with 3 illustrative forecast scenarios, reflecting the highlighted risks. All scenarios are discounted a WACC range of 7.5% to 9.4%, which is broadly consistent with the post-tax WACC disclosed in the 2020 RMG annual report of 9%. (Point 3 noted might play a key role in where that rate should fall.)

Scenario 1 - Pre-COVID reversion. In this Scenario, that I personally believe is a reasonable but conservative scenario, I assume that the trend in revenues and margins which existed pre COVID would gradually be reverted to. This results in an implied share price value of between £3.80 to £5.20.

Scenario 2 - Analyst forecasts to 2023, followed by terminal growth in earnings of 2%. This scenario, which I would consider to be an upside, uses analyst forecasts up to FY23, before growing revenues at a terminal rate of 2%. This results in an implied share price value of between £9.40 and £12.50.

Scenario 3 - This is Scenario 1, but with increased operating expenses reflecting the risk of cost pressures. I'd consider this to be a downside scenario. This results in an implied share price of £3.50 to £4.80.

These scenarios are summarised by the following charts:

You can download and edit my model as desired here:

rmg-dcf-model-230122Download

Closing thoughts:

In my opinion, on balance, the RMG share price looks like decent value, but for the time being doesn't look like a 100% home run, because I think the analyst forecasts are quite optimistic in context with historical performance.

The share price has dropped c.9% in the last month, and if it drops even further then this could be a good one to pick up. For now, I'm sitting on the fence (and to be honest I'm already fully invested at the moment), but I'll be keeping a close eye on RMG. Conclusion: WATCH.