Holding - Anexo Group Plc (LSE:ANX) model update (free download)

Holding - Anexo Group Plc (LSE:ANX) model update (free download)

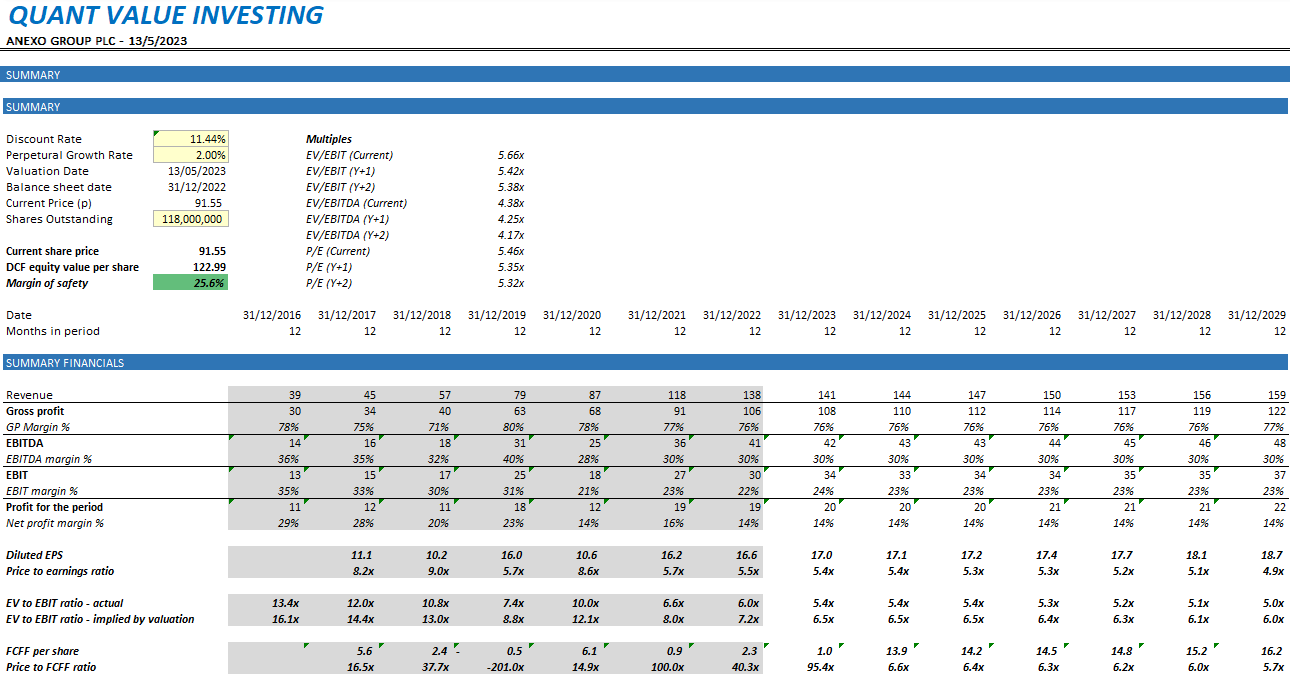

Key facts: 26% margin of safety, 5.66x EV/EBIT, 6.46x P/E, 0.74x P/B, 12.4% 5yr Avg ROIC

Since the last update in April, specialist integrated credit hire and legal services provider Anexo Group Plc has had the CFO resign, the FY22 results released, and the share price decline by c.20%. A lot to take in, but the valuation is still compelling from my point of view.

CFO resignation

CFO Mark Fryer has resigned, but the company has said nothing on the matter regarding the reason for his departure, and given he was only CFO for 9 months, this makes me nervous. The company would do well to bring clarity to the situation, for now, Gary Carrington, who seems reasonably experienced, has been named interim CFO.

FY22 results

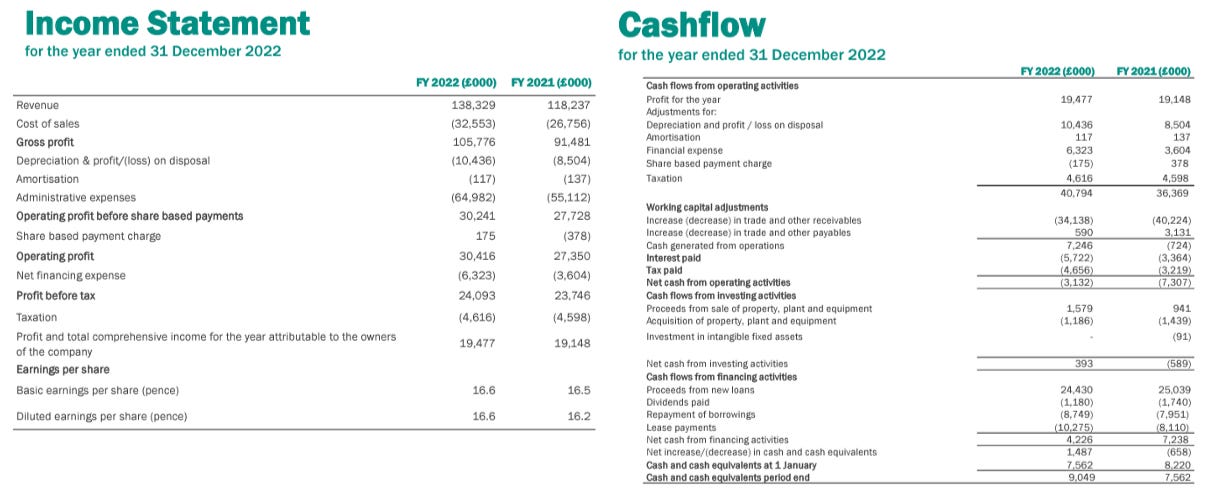

In terms of the performance for the year, they were fine. They were neither disastrous nor exceptional, operating profit did increase 11% YoY, only for increased finance costs to pull back net profit for the year to be flat on the previous period.

The key concerns I have are:

The outlook guidance given by the exec chairman on prospective growth: “The implementation of the Strategic Review means that profit growth for FY2023 is likely to be constrained but there will be an increased return on capital employed. If appropriate, the Group intends to emphasise the progressive dividend policy adopted at flotation. I continue to have great confidence in the Group's strategy and look to the future with continued optimism.” - Alan Sellers (Exec Chair), FY22 full year results.

The cashflow generation (or lack thereof). The business model is very working capital intensive, and while it has grown at pace, increases in working capital have eaten up all free cashflow. Alan Sellers has highlighted cash generation as a key focus going forward, and considering the reduced growth outlook, there is no excuse going forward: “We continue to be excited by the opportunities within Housing Disrepair, which has more than doubled its case portfolio during the year, as well as fresh activity on emissions claims. A focus on prudent case management will enable the Group to concentrate on cash generation and a reduction in overall debt during FY2023.” - Alan Sellers (Exec Chair), FY22 full year results.

No meaningful update on the VW class action.

Perhaps I’m doing ANX a disservice, and I’ve let the market sentiment influence my interpretation of things, the rose tinted view of the world would be to say that the fundamentals are strong, and it’s just the investor communications that have been poor. Nevertheless, prudence always takes precedence in these matters, and as such I have increased the conservatism in my forecasts.

Model update key facts (free model download below):

Due to disappointing guidance coupled with lack of explanation around CFO resignation, I have updated my model to reflect to ex-growth valuation, with only 2% inflationary increases in revenue now assumed

Fair value estimate at 123p (previous: 153p), giving margin of safety c.25.6% (previous: 26.0%)

WACC applied: 11.44% (previous: 11.35%)

EV/EBIT (CY): 5.66x (previous: 6.01x)

P/E (CY): 6.46x (previous: 6.56x)

P/B: 0.74x (previous: 0.96x)

12.4% 5yr avg. ROIC (previous: 12.7%)

Financials Summary

Want to apply different assumptions? Download the model for yourself!

Questions or comments?

Business background

UK company offering credit hire services & legal services to victims of non-fault vehicle accidents.

The company, based in Liverpool in the UK, operates a business model whereby they assist in legal claims associated with non-fault vehicle accidents, and it specializes in impecunious legal claims. An impecunious claim in this context essentially means that the party making the claim does not have the financial means to source a replacement vehicle (think of the scenario in which a local tradesman gets into an accident, and can’t afford to purchase a replacement vehicle which they need in order to work).

The services offered by Anexo in this scenario are twofold: 1) Anexo will assist the claimant in sourcing a replacement vehicle via a credit agreement (this part of the business is called EDGE), and 2) Anexo will process the legal claim against the relevant insurance company to resolution (through its wholly-owned firm of solicitors Bond Turner). To illustrate, this diagram was provided in the Anexo year-end results:

Anexo charges fees associated with both the credit agreement in place with respect to the vehicle, and fees associated with processing the legal claim. The company operates on a “no win, no fee” basis, and therefore a key risk to the business is the success rate of legal claims undertaken. However, a good thing about this area of the legal sector is that the cases are high volume and low value, meaning the risk is well distributed and the cases are typically very standard in nature. As such the failure rate when cases go to trial is below 2% and in fact the vast majority of cases are settled before trial.

The main area of weakness that is inherent in the business model is its vulnerability to further changes in the law. The existence of the business is predicated on a series of House of Lords rulings which set precedents for what rights impecunious claimants have in a vehicle accident situation. Though the leading case with regards to this dates back to 2003 (Lagdan vs O’Connor, https://publications.parliament.uk/pa/ld200304/ldjudgmt/jd031204/lagden-1.htm), further developments continue to unfold (https://www.blmlaw.com/news/to-be-or-not-to-be-impecunious-that-is-the-question), and there is a risk that further developments significantly damage the ability of Anexo to earn revenue.