How Many Stocks Should You Own?

How Many Stocks Should You Own?

(Portfolio) size isn't everything...

Before you continue, I just want to thank all of you for your support, every reader is well appreciated! Know someone else who might also enjoy our work?

When it comes to portfolio size, there’s a whole spectrum of views on the subject, and the battle looks destined to wage on indefinitely. In this article, we’ll look at the pros and cons of either end of the spectrum, and I’ll offer up my two cents on the matter.

First though, a quick show of hands…

In one corner, we have the conviction crusaders (remember that guy on twitter who was 120% net long GOOG 0.00%↑ , I think he’s deleted his account now, hope he’s ok). Conviction crusaders insist that there is practically no such thing as risk in a stock, provided enough research is done and conviction (i.e. confidence) is high. For these folks, more than 5 stocks is a drag on precious time which could be spent finding and misapprehending Charlie Munger quotes. Here’s a fan favourite:

“The whole secret of investment is to find places where it's safe and wise to non-diversify. It's just that simple. Diversification is for the know-nothing investor; it's not for the professional." Charlie Munger.

In the opposite corner, we have the diversification establishment. The old school asset management industry view that diversification is the cornerstone of risk management. Some ‘experts’ recommend portfolio sizes of 60 in order for the full benefits of diversification to be obtained (I suspect such large portfolio sizes merely serve as a barrier to entry so that their services are required in the first place).

Diversification & risk

The purported benefits of diversification are in relation to risk. Modern financial theory asserts that total risk is comprised of company specific risk and systemic risk, which we’ll look at in turn. In this context, by “risk”, I mean the variability in returns.

Company specific (uncorrelated) risk

The benefit of diversification which is cited is that it reduces company specific risk. Company specific risk is risk which is unique to a specific stock, it is uncorrelated with the risk associated with other stocks in the portfolio. This means that every additional stock we own in a portfolio reduces this risk, provided that the company specific risks of each stock are indeed uncorrelated.

It’s worth pointing out I believe, that however you may read Charlie Mungers quote, no matter how much information you have about a company, this company specific risk will exist. I will say though that a heightened level of knowledge may allow us to better measure/understand this risk.

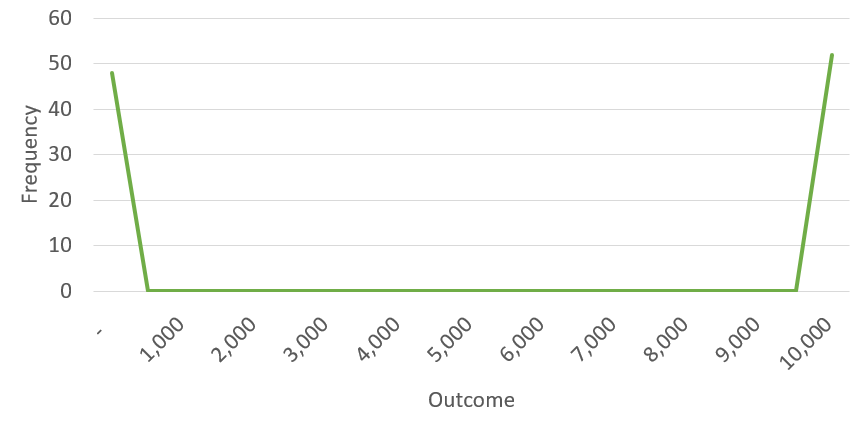

To illustrate why diversification does indeed reduce this risk, imagine you flip a single unbiased coin (a single stock portfolio). If it lands tails, you get £10,000. If it lands heads, you get nothing. The expected return (or average return) of a single coin flip is £5,000 (50% x £10,000 + 50% x £0), however there is a 50% chance that you’ll get nothing. The probabilities are skewed towards the extreme outcomes:

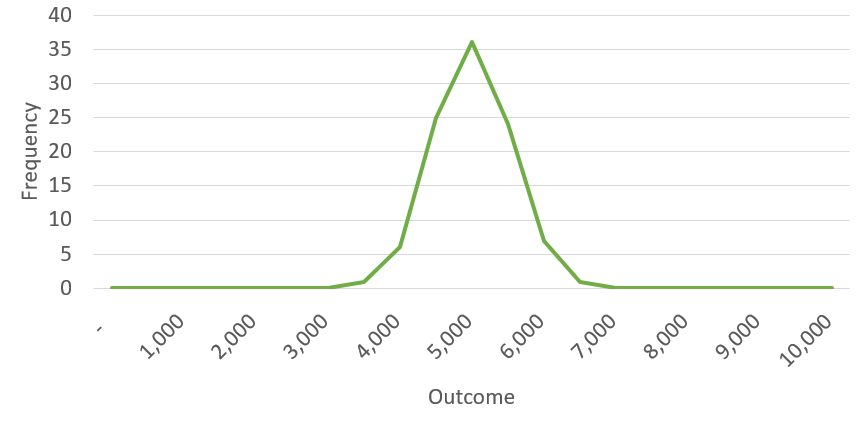

Now imagine you flip 100 unbiased coins at once (a 100 stock portfolio), but instead of a £10,000 wager, the wager is £100 per coin. The expected return is still £5,000 (100 x (50% x £100 + 50% x £0), however this time the outcomes are skewed towards the expected return (in this case in a bell-shaped curve), here are the results of a random sample of 100 of such flips:

The reason the curve looks like this is because the results of each coin flip is uncorrelated. This is what we mean by diversification reducing company specific risk.

Systemic (correlated) risk

Systemic risk refers to risk which is pervasive across investments, it is common between stocks in a portfolio. Because systemic risk is common between stocks in a portfolio, the addition of a new stock to a portfolio does not reduce this risk, and therefore systemic risk cannot be diversified away.

More generally, this principle applies to any risks which are common between stocks (in practice some risks are common between stocks and other aren’t, even if there is an underlying systemic risk which is common among all stocks).

For this reason, I think it is better to think in terms of correlated and uncorrelated risks.

The effect of diversification on returns

Assuming all the stocks held in a portfolio are entirely uncorrelated beyond the underlying systemic risk, and that each stock has the same variability in returns, the following chart shows the total variability in returns of the portfolio depending on the number of stocks (based on excel random number sampling):

The graph shows that the majority of the benefits of diversification are felt by the time the number of uncorrelated stocks reaches 10. The benefits are diminishing after this and beyond 20 stocks, there is little additional benefit.

There is a big a caveat with this conclusion, which is of course that this assumes the stocks held are uncorrelated with each other in their specific risks. The more nuanced conclusion to take from this is perhaps that we should apply it with respect to each specific risk factor.

If we want to get the benefits of diversification associated with holding X uncorrelated investments, we should make sure that for each key specific risk factor, there is at most 1/X % of the portfolio exposed to this risk.

If we want the diversification benefit associated with 10 uncorrelated stocks, we’d make sure that no more than 10% of the portfolio is exposed to any 1 specific risk. E.g. is more than 10% of portfolio value exposed to the tobacco industry? Is more than 10% of the portfolio concentrated in companies located in Kenya?

All that being said, generally speaking, the more companies held, the greater the diversification benefits. To take this to the extreme, the greatest diversification benefits would come from holding an index fund.

The trade off

But diversification isn’t everything. The whole point of holding individual stocks, I would argue, instead of an index fund to begin with, is because we believe that the stocks we hold are likely to generate greater risk-adjusted returns than can be achieved by the market as a whole (i.e. we believe we can beat the market).

We want company specific risk precisely because we believe the stocks we’ve picked will beat the market. This is where the quote from Charlie Munger on diversification comes in.

The reality of investing in this way is that there are other limiting factors which impact the number of stocks we should hold. Clearly, the larger the number of stocks you own:

the more difficult it is to effectively monitor and assess how they are performing

the more difficult it is find enough good opportunities in the first place

In other words, the more stocks we have in a portfolio, the greater the risk of error from us as investors in maintaining & identifying the right opportunities and monitoring specific company performance and risk.

Ask yourself the question, how many companies can I truly track closely, and how many truly exciting opportunities am I likely to find?

Conclusion

In the real world, I want to achieve the greatest level of diversification possible without compromising the diligence with which I’m able to track my investments, and the quality of the investments themselves.

How many companies can I track closely? My gut instinct is probably 10-15, certainly no more than 20 companies.

How many uncorrelated companies should I hold to get the benefits of diversification? Looking at the graph again, personally I’d say at least 8, more than 10 being ideal. In other words, no specific risk factor should have an exposure more than 12.5% of portfolio value (1/8), ideally it would be no more than 10% (1/10).

Conclusion: I’m leaning closer to the conviction crusaders than the diversification establishment, but I’m not taking it to the extreme. My rule of thumb: no more than 10% exposure to any one company or specific risk, but no more than 15 stocks in total.

Now, do you still feel the same way as before? Let’s have another show of hands…

Thanks for reading

Eddie