MODEL UPDATE (SELL @265p): Manolete Partners Plc (free download)

MODEL UPDATE (SELL @265p): Manolete Partners Plc (free download)

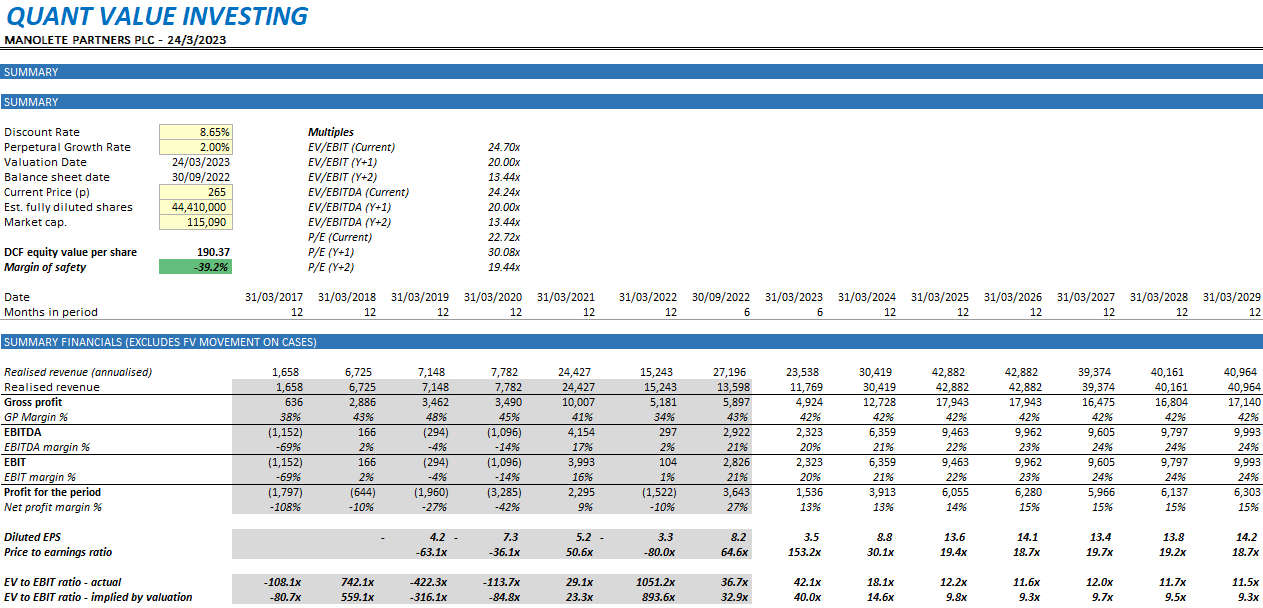

Key facts: 40% overvalued, 24.7x EV/EBIT*, 22.7x P/E*, long-term ROIC* <8% *adjusted to exclude FV accounting adjustments applied to cases

Manolete Partners Plc (MANO) is a specialist insolvency financing business based in the UK (full business plan explanation below).

Historically it has applied fair value adjustments to cases it has invested in when calculating earnings.

Following revising my modelling approach to exclude FV adjustments and focus solely on cashflow generation, it is hard to see how this business will generate enough cash to be viable at this valuation, despite negative economic conditions likely to increase insolvency cases.

Sold @ 265p.

Model update key facts (free model download below):

Fair value estimate at 190p, overvalued by c.39%

WACC applied: 8.65%

EV/EBIT (CY): 24.7x

P/E (CY): 22.7x

Long-term ROIC sub 8%

Financials Summary

Want to apply different assumptions? Download the model for yourself!

Questions or comments?

Business background

Manolete Partners Plc (AIM:MANO) is a specialist insolvency litigation company, based in the UK and listed on the alternative investment market. The company earns its revenues buy either funding or outright purchasing legal claims related to business insolvency (i.e., where businesses fail and there are disputes between various parties as to who owes whom what).

Essentially the company seeks to identify legal claims that have a high probability of success before taking an interest in the claim by either buying it outright or through a funding arrangement. The company therefore invests in legal claims, bearing the risk that the claim is unsuccessful, and seeks to earn a return on these investments through successful claims & case settlements. As such the company is essentially an investment company. Insolvency cases are the only kind of claims that can be purchased by a third party due to a specific exemption in the law.

This a kind of business activity is unfamiliar to most, so it is worth going through how these cases work step by step. The company provides quite comprehensive examples and explanations of how these claims work on the company website, however to sum it up in a few words:

Manolete works in a three-way partnership with insolvency practitioners (‘IPs’) and the lawyers of the IPs. The role of the IP is to oversee the bankrupt business, and attempt to recover as much as possible for the various creditors of the company. Part of this process sometimes involves making legal claims against counterparties to recover funds or assets. As an example, a company may have unlawfully transferred assets to an external entity prior to bankruptcy (for example, inappropriate loans to directors, transferring of property to another entity on non-commercial terms, etc).

The IP will seek to make a claim on behalf of the company to recover funds from the relevant counterparty, however this requires upfront investment to realise the recovery (e.g. expensive legal costs). This is where Manolete comes in. Manolete will either purchase the legal claim outright or provide funding of the claim, taking a share of the gains from successful claims.

In terms of the chronology of a case:

An IP or Lawyer, with whom Mano have built relationships, will discuss a potential case with Mano;

Mano will assess the potential case on a cost vs benefit basis, with the investment committee approving any new cases. As such Mano has staff with experience and knowledge in the area to determine which cases are worth pursuing;

Purchase or funding agreement is made;

The case is pursued, with the case being settled out of court in many cases, but taken to court for judgement if necessary;

If the case is successful, Mano will receive it’s share of the net proceeds. If the case is unsuccessful, Mano will receive nothing, and any costs incurred in the case will be absorbed as an expense.

Market leader in the growing TPF market segment

In the litigation funding market, there are three primary options for those looking to fund their claim:

Conditional Fee Agreement (‘CFA’). This is commonly referred to as ‘no win no fee’, where the fee charge by the relevant solicitor is dependent on the outcome of the case.

After The Event (‘ATE’) insurance. ATE insurance is a type of legal expenses insurance policy that provides cover for the legal costs incurred in the pursuit or defence of the litigation and arbitration.

Third Party Funding (‘TPF’). This is the type of funding which is offered by Mano, where funding or outright purchase of legal claims occurs.

Mano does not use any CFA or ATE agreements in its cases (this is due to the high costs involved), and as such Mano bears 100% of the costs associated with all of its cases. This is the primary risk that the company therefore faces.

Manolete partners currently has a market share in the TPF market of 67% (up from 52% in 2016), and is therefore the market leader in the segment. Despite this, TPF still only makes up a small minority (14%) of the total litigation market of c.£1.5bn in claims (and c.£750m in recoveries) each year (up by 50% in the last 5 years), and therefore there is clear scope for further growth.

In 2016 a change in the law with respect to legal costs came into effect for insolvency litigation cases. The Jackson Reforms (https://hsfnotes.com/litigation/jackson-reforms/conditional-fee-agreements-cfas-after-the-event-ate-insurance/) effectively reduced the amount of legal costs which can be recovered from the opposing party in CFA/ATE agreements. The new rules came into play for most types of litigation in 2013 but these only became active for insolvency cases in 2016:

“Since 1 April 2013, where parties fund their litigation via conditional fee agreements (CFAs) and/or after-the-event (ATE) insurance, the CFA success fee and ATE premium are no longer recoverable from the losing opponent if the case is successful. Parties can still enter into CFAs and take out ATE insurance to fund their litigation, but have to bear the additional costs of doing so.

Parties can enter into a CFA with their lawyer, where the lawyer is paid up to double the normal fee if the case is won and nothing, or sometimes a discounted fee, if the case is lost. The uplifted fee is called a success fee, and it is capped at 100%.

Parties can also take out ATE insurance to cover their risk of having to pay the opponent’s costs, as well as their own disbursements, if they lose the case. ATE policies are sometimes available with “deferred and self-insured” premiums, meaning the insured party does not have to pay the premium until the end of the case, and does not have to pay it at all if the case is lost – ie the insurance kicks in to cover the cost of the premium itself as well as the adverse costs if the case is lost.

The crucial feature of this system as it applied before 1 April 2013 was that both the CFA success fee and the ATE premium were recoverable from the opponent if the case was successful. As recommended by Lord Justice Jackson, that is no longer the case for CFAs entered into and ATE policies taken out on or after 1 April 2013.”

As a result of this, the financial incentive for taking up CFA or ATE arrangements has significantly reduced, and relatively this makes the TPF option much more attractive. On the back of this the TPF share of the market share has doubled from c. 7% in 2016 to approximately c. 14% in 2021.

Eddie.