Watchlist - Ultimate Products (Free Valuation Model Download)

Watchlist - Ultimate Products (Free Valuation Model Download)

Key facts: 3% undervalued, 8.3 CY EV/EBIT, 9.8 CY P/E, 22% 5yr Avg ROIC, 7% 5yr Revenue CAGR, management own > 25%

Before you continue, I just want to thank all of you for your support. Every subscriber is very much appreciated!

Summary

I’m on the hunt for new ideas, and my approach to this is to identify companies I like, regardless of price, with the idea being to pounce once they fall into a price range I’m comfortable with.

Any stock ideas to share? Let’s hear them:

UP Global Sourcing Holdings Plc (“Ultimate Products”) may not roll off the tongue, but the Oldham based business has great qualities that, at the right price, I’d be excited to include in my portfolio.

It develops, designs, sources and distributes consumer products, focusing on six product categories: Small Domestic Appliances, Housewares, Audio, Laundry, Heating & Cooling and Luggage. Think toasters, air fryers, vacuums, household products of various sorts.

The companies skillset and competitive advantage has always been quality product development & marketing, with it’s strategy in recent years being to acquire known and trusted brands before fine-tuning their products. It’s recent growth is impressive (revenue up nearly 100% since 2018, profit up nearly 200% since 2018), and it’s continued international expansion offers the possibility of an even brighter future.

The greatest risk for UPGS, in my view, is the impact of cyclical demand for it’s products. For sure, many of their products fit into the non-discretionary category, but then again others don’t (I don’t know how many people will be buying air fryers in a recession). The swing to demand for goods in the COVID era has been a strong tailwind and, although recent results have been resilient, I think there will be pressure on margins and growth in the short-term.

For this reason, UPGS remains on my watchlist, hopefully one day soon it’ll have the margin of safety I’m looking for. Fair Value estimate: 151p (vs 146.5p current price]). Conclusion: watchlisted.

Jump to section

1.Company History

Established in 1997, UPGS was founded by the still CEO Simon Showman. Initially a clearance business buying discontinued and excess stock, Simon was able to grow the business into the full-service sourcing and importing operation that remains today.

During the early 2000s, Simon began to source regular products from countries around the globe such as Portugal, Vietnam and, in time, from China. This led to investment by Lloyds Development Capital, enabling Simon to become the Chief Executive Officer and largest management shareholder in 2005.

As the Company grew, Simon was able to use his increasing knowledge to change the focus of the business in 2014, moving away from own-label and unbranded products to fine-tuning key brands.

The company IPO was in March 2017 and in the time since then the business has nearly doubled revenues and nearly tripled profits, with the acquisition of Salter, the UK’s oldest houseware brand (est. 1760s) which it previously licensed, in 2021 being a notable feather in their cap:

2.Business Model

When is comes to business models, simpler is better. Retail businesses are very easy to get your head around, conceptually at least. The UPGS business model is to develop branded household goods using third-party overseas manufacturers and to deliver them globally for consumers.

Taking a look at the supply/cost side first, the company outsources it’s manufacturing processes, which brings with it pros and cons:

reduced operating leverage, i.e. lower fixed costs, is a benefit in terms of reducing the downside risk to profitability, but conversely it limits the benefit of increased volumes

it means that supply chain management is crucial (this, along with brand strength & product development, are the key barriers to entry for competitors), and we can take comfort from the strong performance of the business in the last couple of years which have been challenging from a supply chain point of view

Despite this the business has done well to expand margins over recent years, and it’s current goal is to push this further with integration of robotics and automation into more of it’s processes:

The company has historically been concentrated geographically in terms of manufacturing (China) which is a risk to keep an eye on, as part of the company’s ‘ESG’ strategy the business has stated it’s intention to identify potential factory locations in other jurisdictions.

Looking at the demand/revenue side, the business operates on both a B2B and B2C business, although B2B is the majority of sales with supermarkets and discount retailers being key segments:

In recent years the focus for the business has been to expand internationally, to allow it’s online channels segment to grow (the growth in this segment in H1 was the saving grace of revenue growth in the half as shown above), and to streamline it’s product development (allowing focus on key products and lower costs):

The elephant in the room in terms of revenue however, in my opinion, is the macro sensitivity of the business, which I’ll come onto in the next section.

3.Outlook

Taking a look at the most recent results, performance for UPGS has held up well. Revenue has ticked upwards 2% and gross margins have remained flat in H1 2023 vs the prior year with easing supply chain pressures being a key positive. Meanwhile there is pressure on operating margins with the key increase in costs coming from labour costs and finance costs. Here's the P&L for the half:

The following chart shows the volume of furniture & furnishings sales in the UK since 2005 (I believe this is a good proxy to use for UPGS' household product mix.

The first thing to notice is that the trend has been strong over the last few years, with enhanced consumer spending on goods being a key reason for the jump in 2020. It would however be a disservice to UPGS to attribute all their success to this wider trend, as it has far outperformed the wider market in terms of growth in sales (c.2x since 2018):

The second thing to notice on this graph is the decline in spend on items of this type in the year that followed the last recession, where volumes bottomed in 2012 even though the recession took place a couple of years earlier. So how did UPGS do during this period during a declining market? The company only listed in 2017 so in order to find out a dig into companies house is necessary.

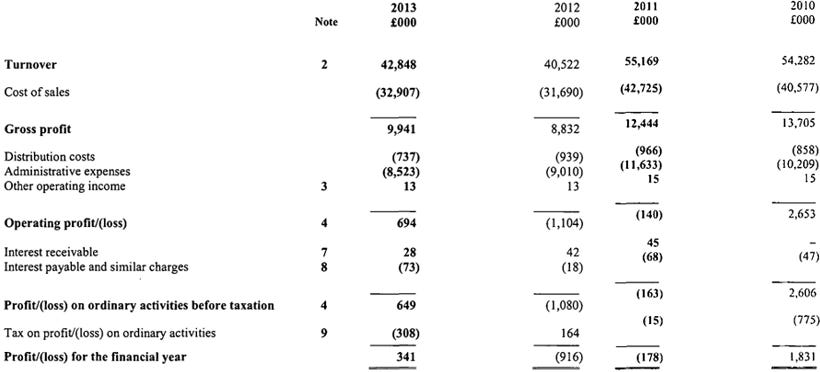

The extract below shows that the business was not immune to this wider market decline, it suffered moderate losses in 2011 & 2012 before beginning to recover in 2013.

It is no great leap to suggest that if a recession does unfold, household product spending will again decline and although UPGS is better placed to weather such an eventuality than in the past, this cyclicality is something we must consider in our valuation.

4.Management

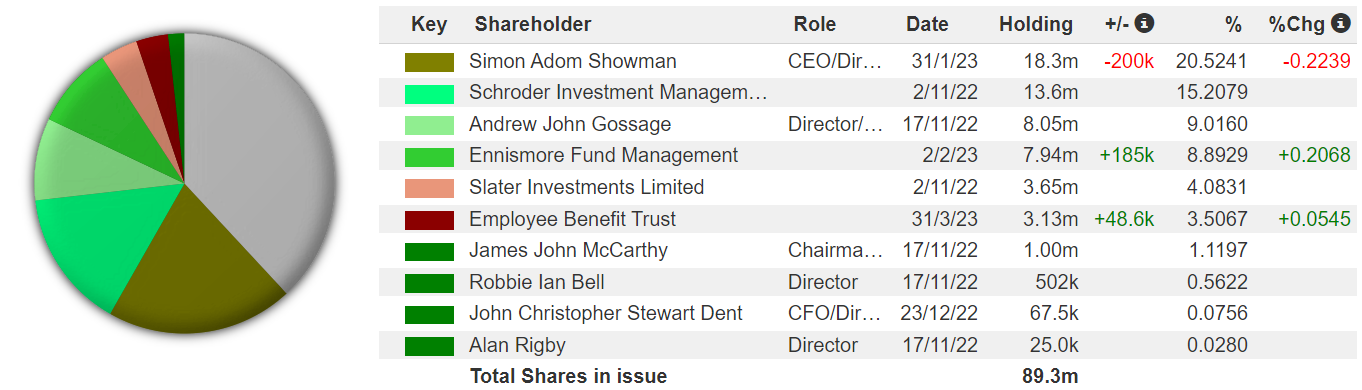

A management team with aligned incentives is a non-negotiable when I'm searching through new potential investments, and that box is decisively ticked when you look at the % ownership the management team hold:

The other key considerations when looking at the management are 1) competence, and 2) longevity. Lets take a look at the executive directors in turn:

Simon Showman (CEO). As mentioned previously mentioned, Simon founded the business in 1997 providing ideal depth of expertise. He remains the lead of the Group’s international expansion strategy and is directly responsible for the key trading functions of sales and buying, continuing to be the driving force behind the ongoing development of the Group. He remains only 49 years old so all being well longevity shouldn't be an issue.

Andrew Gossage (Managing Director). Andrew has been with the company since 2005 bringing a similar level of experience to the table. Whilst Simon oversees trading functions Andrew is responsible for online and non-trading functions (e.g. supply chain, HR, IT, Legal, etc). He was initially appointed as Finance Director but has also held the role of COO and has been the Managing Director since 2014, overseeing a very successful period for the business. Andrew is currently 51 and likewise should have some years ahead of him.

Chris Dent (CFO) - Chris joined Ultimate Products on 4 April 2022. Note his appointment followed Graham Screawn's decision to retire in the second half of 2022 - a new CFO is never ideal for investors but retirement & a managed transition is the best you can hope for. Chris joined Ultimate Products from Franchise Brands plc, the AIM-listed multi-brand franchise business, where he had been CFO since July 2017. He previously spent four years as Finance Director of 7digital Group plc, the B2B music solutions business, and began his career at Deloitte where he was for 10 years. Chris has the requisite experience in businesses in the industry and we can take comfort from he fact that the MD was previously Finance Director. Chris is new to the business and is still young at 42.

The only risk to consider is whether having such experience in Simon & Andrew could bring with it a key man risk. Perhaps not an issue right now but succession is always something to keep an eye on. Otherwise from a management perspective all the boxes are ticked.

5.Valuation

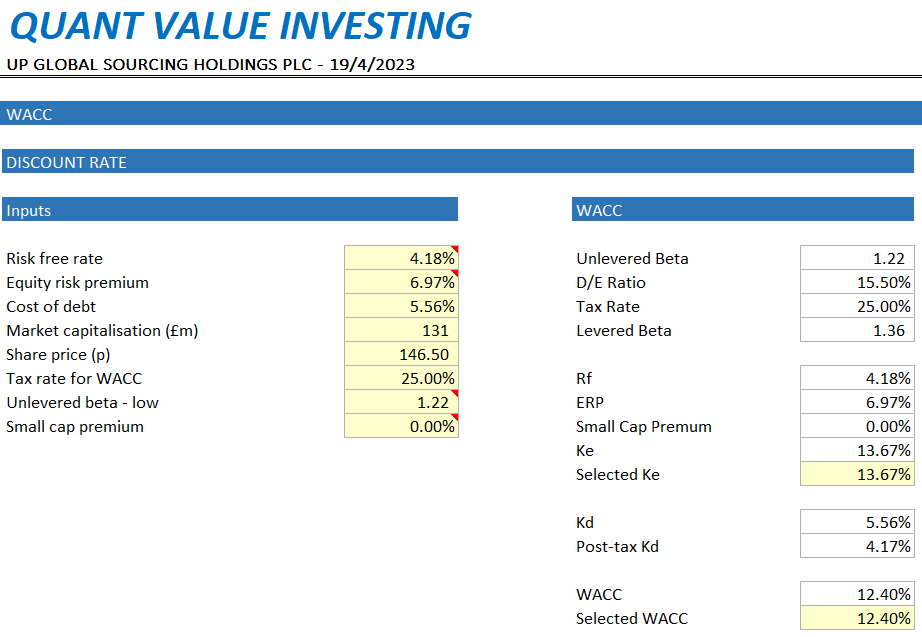

In terms of valuation, I’ve used an enterprise level DCF approach, and I’ve used CAPM to estimate a WACC, utilising Damodaran’s equity beta for general retail & country risk premium to calculate this. Cost of debt & D/E ratio is calculated using the H1 2023 report.

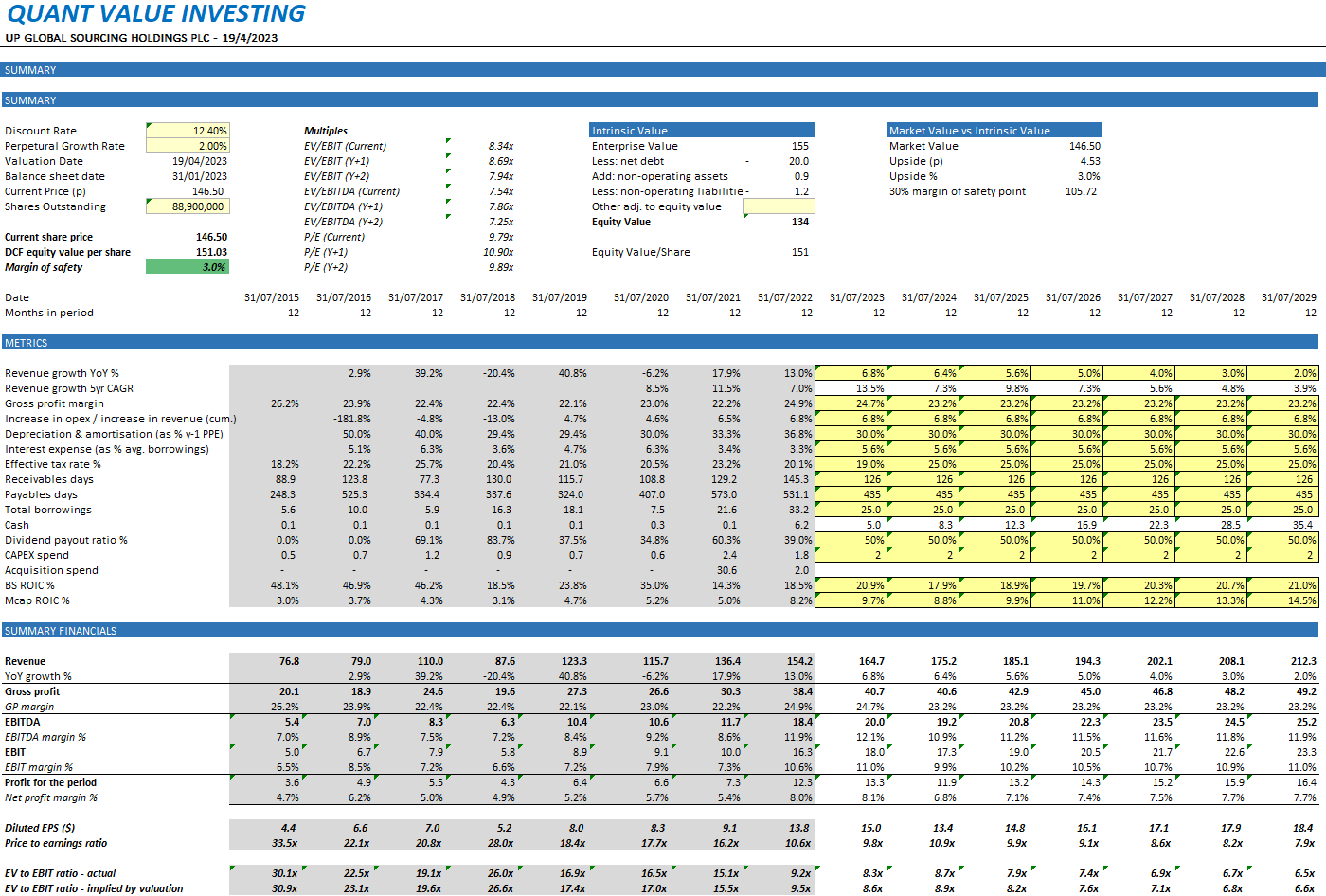

Conclusion: WATCH. Fair value 151p, target buy range 100p - 110p.

Discount rate

The WACC I’ve calculated is 12.4% which is quite hefty, but given previous discussion of cyclicality and rates at the minute I’m comfortable with it.

Financial Summary

In terms of financials I’ve tried to keep it relative conservative (they are more conservative than analyst forecasts which are shown on a separate tab in the model), with a reversion to slightly lower margins and slowing revenue growth:

Want to apply your own assumptions? Download the model.

Thanks for reading!

Eddie.