Watchlist - Focusrite (LSE:TUNE)

Watchlist - Focusrite (LSE:TUNE)

Key facts: 8% overvalued,15.1x CY EV/EBIT, 20.6x CY P/E, 18.1% 5yr CAGR, >20% 5yr Avg ROIC, management own > 25%

My portfolio positioning is currently heavily weighted towards cash / money markets, which more than anything reflects my feelings of gloominess towards the macro environment. I’m a believer in the seemingly old fashioned idea that the withdrawal of inflation inducing stimulus, and the associated reduction in inflation, will bring with it temporary economic pain.

Just as excesses of COVID spending were a boon for various consumer discretionary businesses, so to will economic hardship prove detrimental to these same businesses. But it will be temporary pain, and with that brings an opportunity to seek out the quality enduring businesses in their moment of temporary adversity.

“Experience teaches that the time to buy preferred stocks is when their price is unduly depressed by temporary adversity. (At such times they may be well suited to the aggressive investor but too unconventional for the defensive investor.)” - Benjamin Graham

Whilst there are no guarantees a given company will reach an unduly depressed price, the best odds one can give themselves in finding such opportunities is the obtain a good shortlist of desirable companies, in the hope that a few might become viable investments. To this end I recently wrote about Ultimate Products (“UPGS”):

Summary

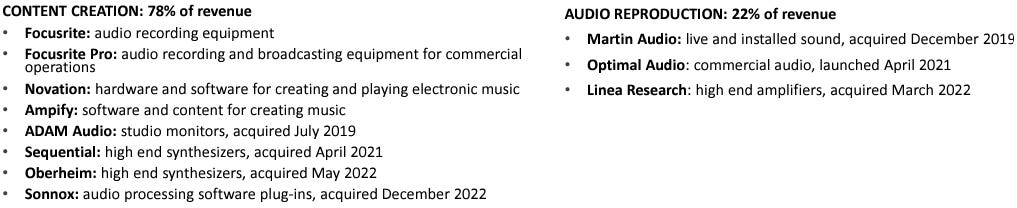

Today, however, we’re here to talk about Focusrite Plc. Focusrite (LSE:TUNE) is an English music and audio products group based in High Wycombe, England. The Focusrite Group trades under eight brands: Focusrite, Focusrite Pro, Martin Audio, ADAM Audio, Novation, Ampify Music, Optimal Audio and Sequential.

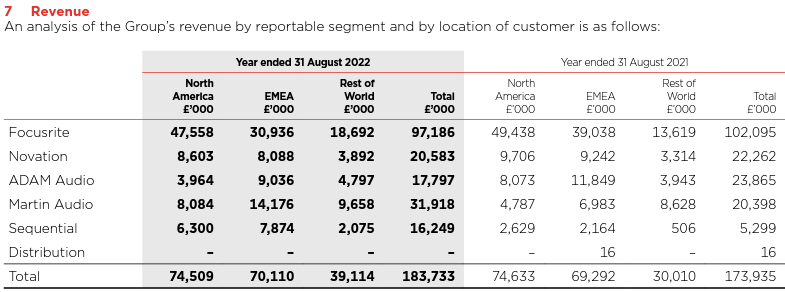

The lion share of the business revenue is generated from the sale of equipment, of which it offers a large variety. As a user of music studio products myself, it’s brands have a good reputation of quality. In recent years, the business has also diversified into more live music & events offerings, which now account for c.22% of revenues. It also has the benefit of being geographically diversified with revenue split c.40% US, c.40% EMEA, and c.20% RoW.

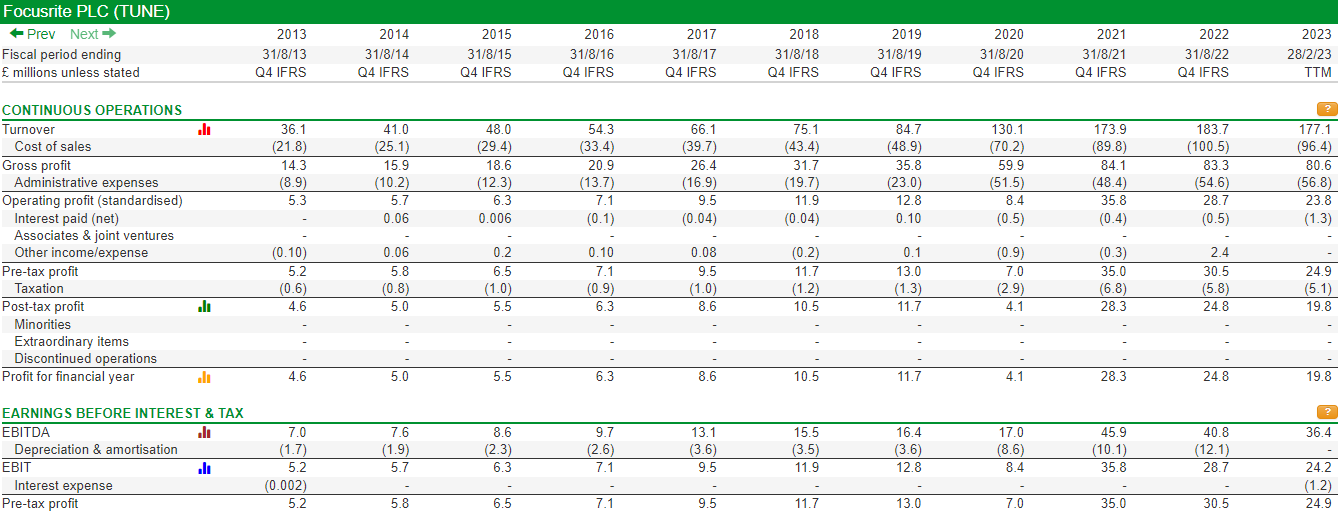

Focusrite had enormous success during the pandemic era as bedroom music producers and nothing-to-do hobbyists descended onto their array of music products, with revenues and profits more than doubling since 2019, however I am at pains to point out that it’s successful track record of healthy margins & high growth long pre-dates the pandemic, reflecting the wider trend of music production becoming more widely accessible for amateurs.

The share price has been for a full round-trip since 2019, with it’s share price falling c.70% since it’s peak in 2021. It begs the question, is this business really worth LESS than it was pre-pandemic?

Outlook

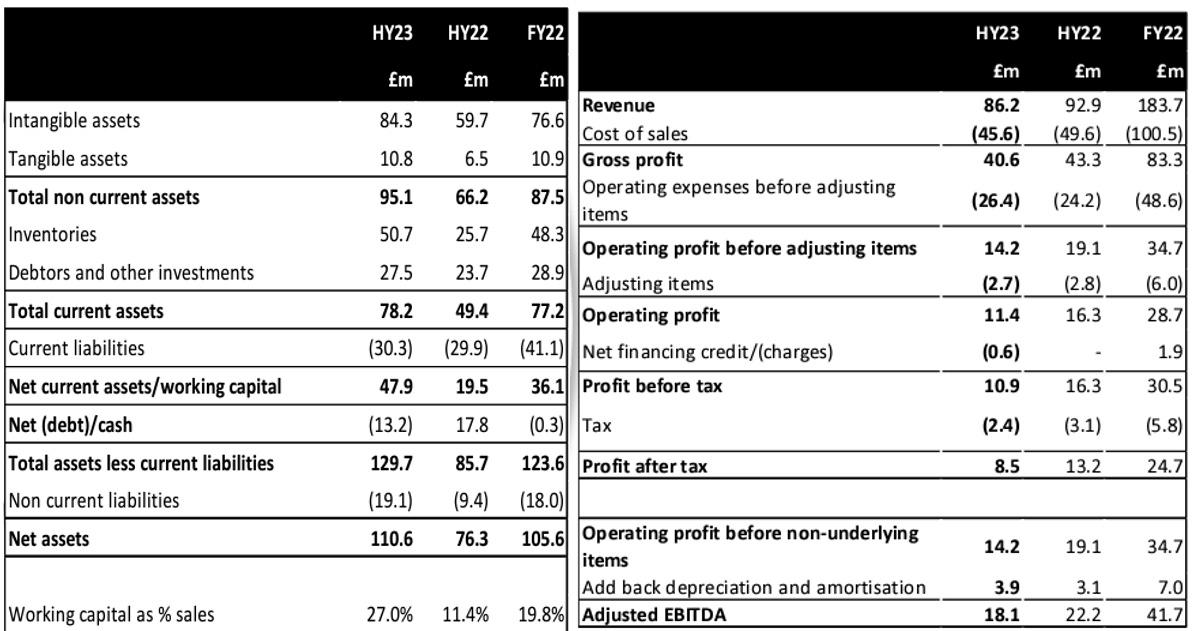

Drawing particular attention to the latest half-year report, it is clear that demand is slowing. Although gross margins held up well, this was at the expense of revenue growth, and one tell-tale sign of slowing demand which investors picked up was an increase in inventory. Management were keen to point out that the increase in inventory was merely the normalisation of inventory levels following recent supply chain constraints and exceptional demand.

I don’t think I believe that, but even so on a cold read the results don’t scream disaster whatsoever. The business remains highly profitable and I think the biggest reason that the results irked investors so much is that the manner of delivery from the CEO & CFO was very nonchalant, quite unconcerned frankly.

To consider this business as an investment on the basis that it will see through a temporary difficult period, it’s important to think about failure risk and balance sheet resilience. From a balance sheet/financial strength point of view, the business has a low level of leverage (less than 1x EBITDA per the HY) and given margin levels this is a remote risk in my opinion.

Even so, I think the next couple of years will be a challenge.

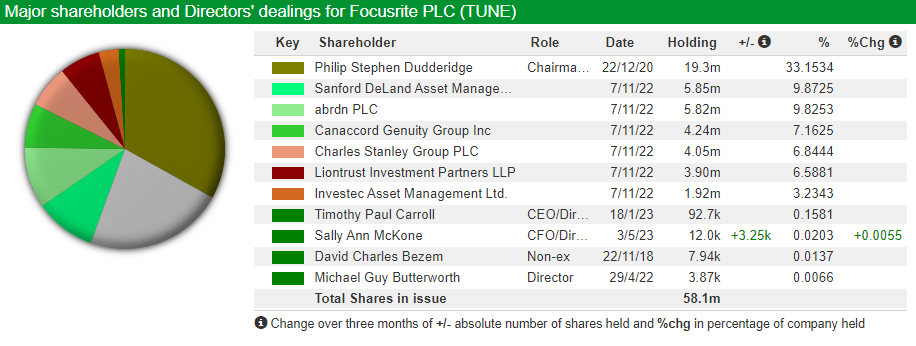

Management

The management team is an interesting one in this case. The business was founded by the Chairman Philip Dudderidge who still holds a whopping 33%. This certainly creates good alignment with him, but CEO Tim Carroll and CFO Sally McKone, who perhaps are really at the wheel, have much more modest stakes in the business.

I would prefer it if the exec directors had bigger stakes, but at least the current incentive plan in place pegs director rewards to EPS targets rather than any share price metric (my preference by far), meaning continued improvement in fundamentals should be front of mind.

One thing to note is that the large founder ownership and other institutional ownership means less than 25% of the companies shares are ‘effectively’ freely traded, and this coupled with the fact that the chairman has, understandably, been gradually been selling down his share in the business over time, has from a technical standpoint been a big drag on price performance and a driver of volatility.

Valuation

In terms of valuation, I’ve used an enterprise level DCF approach, and I’ve used CAPM to estimate a WACC, utilising Damodaran’s equity beta for & a mixed country risk premium to calculate this. Cost of debt & D/E ratio is calculated using the H1 2023 report.

Conclusion: WATCH. Fair value 500p, target buy range 325p - 375p.

Discount rate

The WACC I’ve calculated is 12.2% which is quite hefty, but it’s broadly consistent with the pre-tax discount rates disclosed in the accounts for impairment purposes (10.8% for the core Focusrite CGU) and given cyclicality and risk free rates at the minute I’m comfortable with it.

Financial Summary

In terms of financials I’ve tried to keep it relative conservative (they are more conservative than analyst forecasts which are shown on a separate tab in the model), with a reversion to pre-pandemic margins and slowing revenue growth:

Want to apply your own assumptions? Download the model.

Thanks for reading!

Eddie.