Watchlist - Argentex Group Plc (LSE:AGFX) Model Update (Free Download)

Watchlist - Argentex Group Plc (LSE:AGFX) Model Update (Free Download)

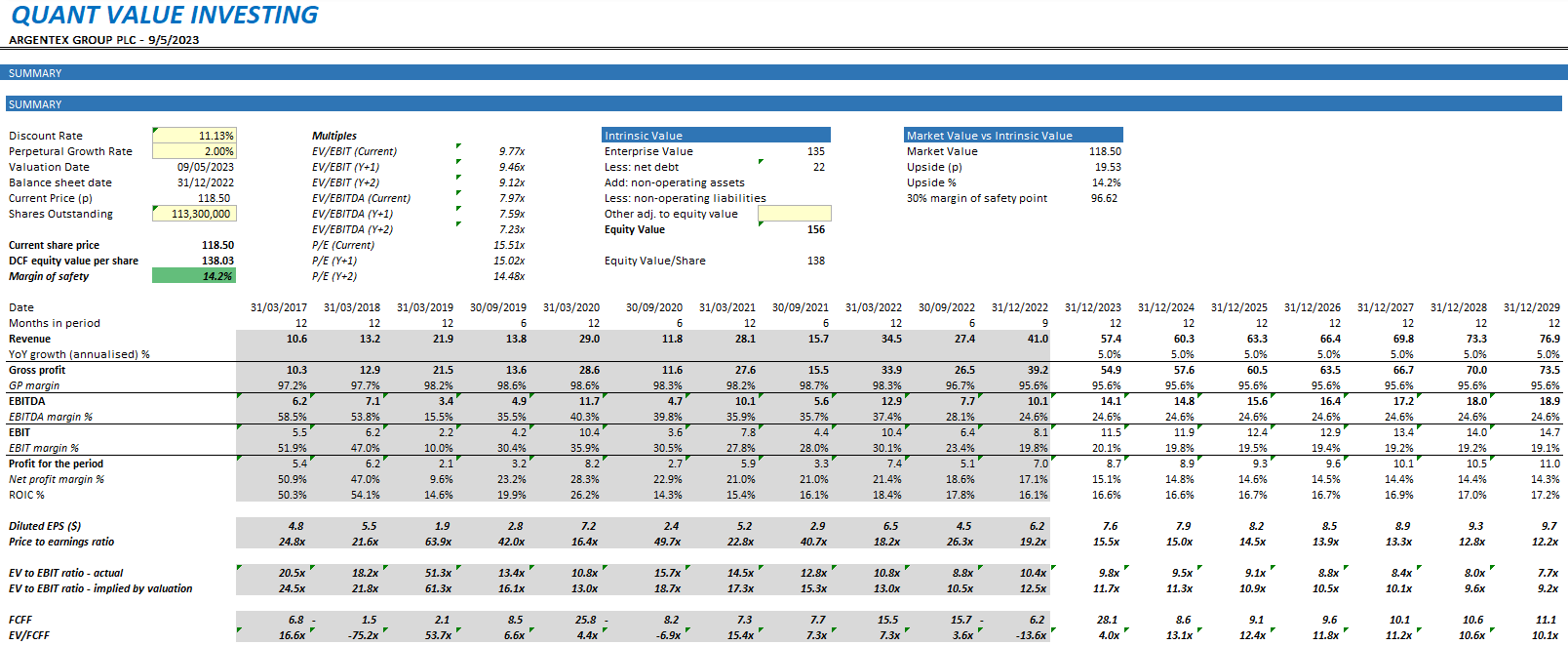

Key facts: 14% margin of safety, 9.8x FY23 EV/EBIT, 15.5x FY23 P/E, >20% 5yr Avg ROIC, >25% 5yr Revenue CAGR

AGFX is a no-risk FX broker who provide FX instrument solutions for non-speculative clients. In plain English, the company arranges FX contracts for businesses, who need them for their own risk management purposes (as opposed to speculative purposes), and it avoids taking on any proprietary position in FX instruments.

I originally bought the share at 74p in April 22, and sold earlier than expected for 118p in Jan 23, at which point I’d concluded that most of the upside had been realised. I didn’t sell the share because of any issue with the business, I still think it’s a good business, so it’s certainly on the watchlist for now.

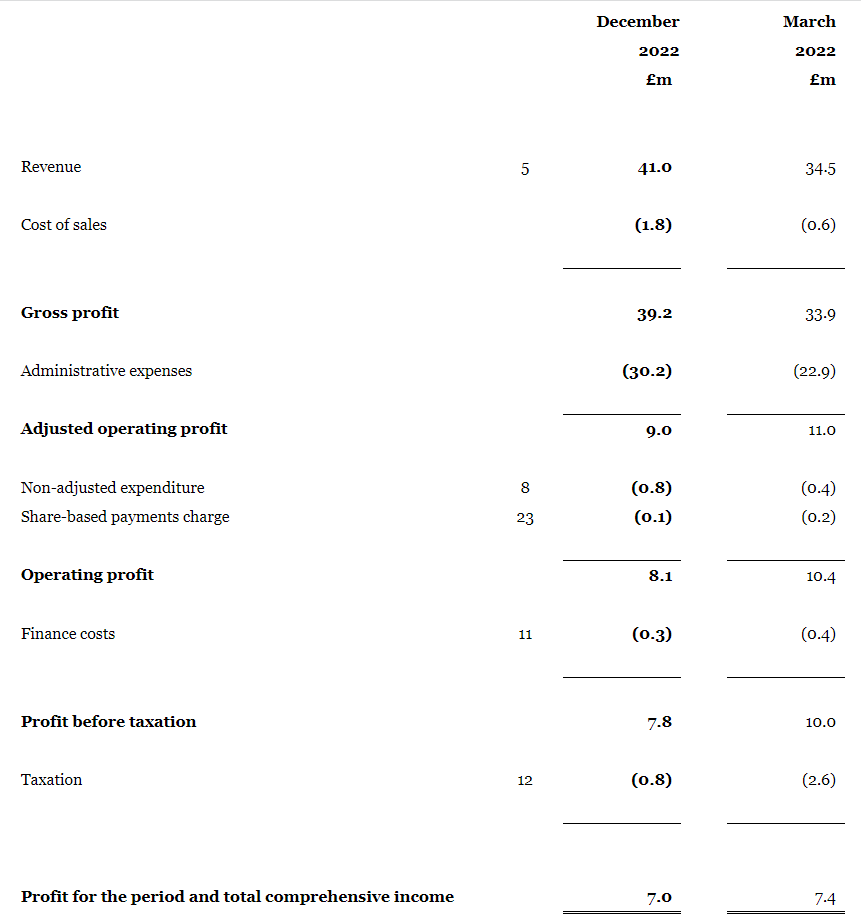

In terms of updates since that time, the company released it’s results for the (9 month) period ended 31/12/2022, after it announced it was changing it’s reporting date from 31/03, the given reason being for greater ease of reporting in context with international expansion. This change does muddy the waters slightly in terms of analysing figures, but the overarching takeaway from the latest results are:

revenue growth has been strong, and progress on international expansion in Europe & Australia appears positive

margins have been squeezed slightly (net profit margin down to 17% from 21%), but remains healthy and cash conversion remains a strong positive

management insist that the expansions into new regions with new product propositions should encourage wider margins, but this remains to be seen so far

there was some concern over whether recent bank instability has impacted AGFX, the message from management was that, as a competitor to banks FX services, it actually stood to benefit and acquired clients during that period

The thesis for AGFX is effectively unchanged from my perspective, it has an excellent track record of growth and return on capital, it has a net cash position, it has a large management ownership, and a runway for further expansion. The key risks remain whether management will sacrifice profitability in pursuit of growth, as well as the overarching business risks relating to counterparty settlement risk & variation in transaction volumes. As such, it’s really a question of price.

Full details in the original write-up:

Model update

Model update key facts (free model download below):

Fair value estimate at 138p, giving margin of safety c.14%, not quite enough for me to consider taking a position

WACC/Ke applied (debt-free): 11.13%

>20% 5yr historical avg. ROIC

>25% 5yr historical revenue CAGR

Want to apply different assumptions? Download the model for yourself!

Questions or comments?